The future of American SVOD lies outside of the US

Squid Game

There is little more to say about Netflix that hasn’t already been said.

There had been slight concerns about the service – which often serves as a barometer for the health of the streaming industry at large – when it suffered two consecutive underwhelming quarters for the first half or 2021.

However, the company has experienced a resurgence in the third quarter of the year. Globally, Netflix added 4.38 million paid subscribers for a total of 213.6 million worldwide, surpassing internal projections of 3.5 million additions.

While there has been no shortage of coverage about the astronomical viewer figures of Korean thriller Squid Game, understated in the reporting of Netflix’s comeback story is the fact that less than a million of those new subscribers came from the US.

Predictably the success of Squid Game has seen growth in Southeast Asia, but the company is clearly diversifying its strategy in order to cater more towards an international audience in what is increasingly becoming a trend for US-based streaming companies.

Going global

Focusing on international audiences is hardly a new thing for Netflix. Its staple content like Stranger Things and Orange is The New Black have had a global appeal as a result of the US being the pop-culture centre of the world, but more and more we are seeing non-English language content prove popular on a global stage.

Years before Squid Game, Netflix’s bought the distribution rights to La Casa De Papel in a move which resulted in thousands of Halloween costumes the world over. Equally, The company has seen content success with series like the German Dark, India’s Sacred Games and the Japanese thriller Alice in Borderland (whose conceptual similarities to Squid Game have seen the series gain a resurgence in attention over the past month).

Dovetailing with an increasing focus on international content are strategic moves in developing markets to access a largely untapped audience for US media companies.

Launch of Disney+’s Star hub in Europe earlier this year is one example of how the company is diversifying its product in different markets

In 2019, Netflix launched its first mobile-only offer for the Indian market (a model later emulated by Amazon in early 2021) and last November offered the entire country a free weekend of access.

It’s not just India where Netflix is experimenting with its distribution model. The company provided a glimpse into its approach in its Q3 letter to shareholders where it highlighted the launch of a free plan for mobile users in Kenya. It explained that this is a move designed to encourage those users to sign up for a paid membership so they can watch Netflix on any device and access more features.

Netflix is by no means alone in its attempts to capture a global market though.

Disney, which this week received a rare stock downgrade, has varied its approach across multiple markets. In the US, Disney’s entertainment streaming services Disney+ and Hulu are clearly defined from one another. In some markets, Disney combines much of the content that is native to Hulu with Disney+ via its Star Hub; while in others Disney offers Star as a completely standalone product.

Much of this product experimentation has taken place in Southeast Asia, where Disney is predicted to surpass Netflix for subscribers by the end of the year.

All of this is to say that there are great potential rewards for US-based streamers to invest in overseas deployment, but there is no one-size-fits-all approach that will prove successful in the long term.

Bored in the USA?

With such a great deal of attention being placed on international expansion, it begs the question of whether the US market – arguably the most mature and crowded SVOD market in the world – has finally reached a saturation point of subscription fatigue.

Take HBO and its complementary streaming service HBO Max. Despite the US-only feature of offering Warner Bros. cinematic releases day-and-date on streaming at no additional cost, HBO’s US subscriber base took a dip in the US during the most recent quarter. This has largely been blamed on the fact that HBO Max left Amazon Prime Video Channels in September, but it is telling that a significant number of subscribers did not feel the need to seek out HBO Max on its own.

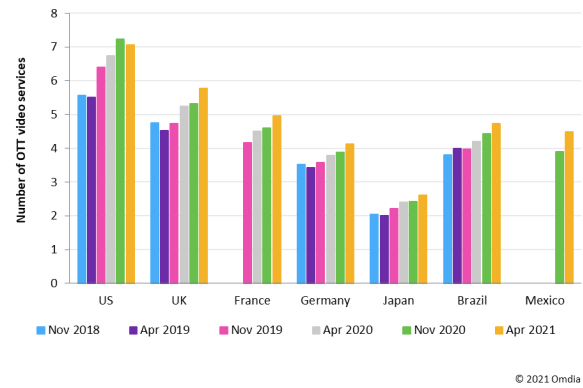

Global, average number of online video services used per online video user by country, Nov 2018–Apr 2021

Omdia earlier this year reported that the US had experienced a drop in the number of online video services used per online video user from an industry high of 7.23 in November 2020 to 7.06 in April. Other markets such as the UK, Japan and Brazil are all still trending upwards.

Despite this, the report goes on to note that the number of online video subscriptions per household had narrowly increased from 3.08 in November 2020 to 3.16 in April 2021 for an 80% household penetration.

This is reflected by the Digital Entertainment Group (DEG), which in August conclusively refuted any notion of subscription fatigue. Consumer spending on subscription streaming rose almost 17% to US$6.3 billion for Q2, and by 21% to US$12.2 billion in the first six months of 2021.

The US is not ‘done’ as a market for growth in the streaming subscription world, and it would be premature to assert that it has hit the fabled fatigue point. However, the US is evidently delivering diminishing returns and major media players are wise to diversify their approach to focus on the international stage.

With WarnerMedia’s HBO Max set to launch in Europe next week, and Disney, Amazon and Netflix all continuing to adopt fluid strategies for various markets, major US players in 2021 know that they need to look beyond their borders for long-term success.