Smart TV makers zone in on advertising opportunity

Maria Rua Aguete (centre) and Thierry Fautier (right) discussing TV OS at the Connected TV World Summit

Smart TV manufacturers are likely to continue to focus on building an advertising business given the superior margins available from this business compared with selling hardware, according to data released by Maria Rua Aguete, senior research director, Omdia, at the Connected TV World Summit in London today.

However, the smart TV ecosystem remains highly fragmented, with multiple suppliers and different OS platforms and big regional variations in which supplier and OS dominates around the world.

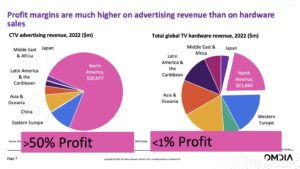

According to Omdia, profit margins from CTV advertising in 2022 were in the order of over 50%, while globally, margins from the sale of TV hardware were less than 1%.

The vast bulk of 2022 CTV ad revenues – about three quarters of the total – came from the US market, totalling about US$20.1 billion. Hardware revenues were more widely geographically dispersed, with the US accounting for about a fifth of the total, roughly the same as western Europe. US hardware revenues amounted to US$21.7 billion in 2022.

The predominance of the US in CTV ad sales is linked to the growth of FAST in the US, where it far outpaces developments in other markets. This is likely to persist, given that FAST is seen to represent and alternative or replacement for basic cable in the US, with its rise intrinsically linked to cord-cutting and the emerging population of ‘cord-nevers’.

Source: Omdia

The smart TV ecosystem remains highly fragmented geographically, according to Omdia.

While Samsung and LG together enjoy a 30% market share (with two thirds of that going to Samsung), the remainder of the global market is divided between multiple players, including Hisense, Xiaomi, Skyworth, Sony, Vizio, Vidaa and multiple others.

There are also sharp contrasts in the division of the market between different smart TV OS depending on which part of the world you are in.

Globally, Android is the dominant smart TV OS, with over 40% of the world market, but that is primarily down to the size of the Chinese market, where Android is dominant thanks to the popularity of manufacturers such as TCL, Xiaomi and Hisense.

The other main OS players are Tizen (proprietary to Samsung), with a 19.8% global share, WebOS and Roku (which is the market leader in the US), Vidaa, Amazon Fire TV and CastOS (Vizio).

The European market by manufacturer is highly fragmented, with no dominant pan-European players. Android overall has the biggest single OS, followed by Samsung and Tizen with a 26.3% share, LG’s WebOS and Hisense’s Vidaa.