After more than 40 years of operation, DTVE is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

IHS: Apple now the third largest set-top box company

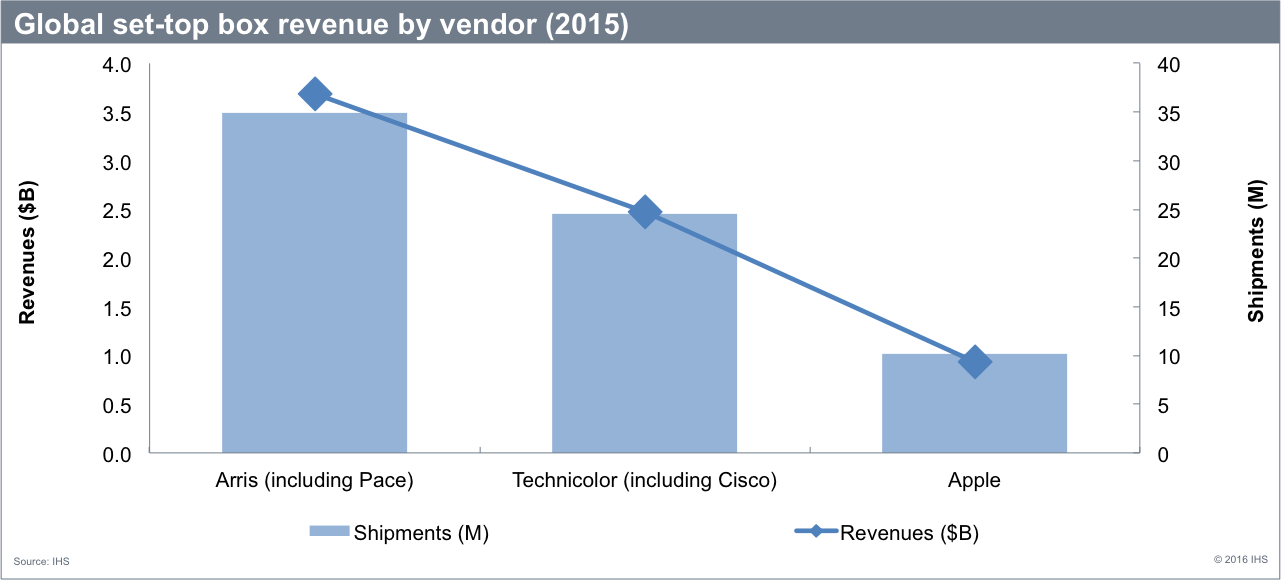

Apple surged to third place in the global set-top box market by revenue last year thanks to the success of its Apple TV device, according to new stats from IHS.

Apple surged to third place in the global set-top box market by revenue last year thanks to the success of its Apple TV device, according to new stats from IHS.

The research firm said that Apple had climbed from ninth place in 2014 to third in 2015 thanks in part to strong growth in consumer retail over-the-top streaming boxes.

Arris and Technicolor, which ranked first and second in terms of global set-top box revenue, were also helped by their respective acquisitions of rivals Pace and Cisco last year.

In terms of unit shipments, IHS said that Apple moved more than 10 million Apple TV boxes in 2015 – the fifth largest volume in the world following Arris, Technicolor, Skyworth and ZTE.

Overall, global set-top box shipments grew 4.8% year-on-year in 2015 to reach 353 million units –driven by internet-protocol television (IPTV) in China.

However, revenue for 2015 fell 5.4% to US$22.2 billion, due to reduced demand for high value STBs in North America, “primarily caused by poor pay TV performance in the region”, said IHS.

Despite this, revenues were up 3.4% quarter-over-quarter in Q4 to reach US$5.7 billion, partially driven by “next generation device launches of Apple, Amazon, and Roku”.

“The STB market has certainly grown since 2007, when Steve Jobs originally described the Apple TV business line as a ‘hobby. Now we’re seeing sales of Apple’s consumer devices in the millions, which has catapulted the company ahead of leading STB manufacturers that ship to pay TV providers,” said Daniel Simmons, director of connected home for IHS Technology.

“The new positioning of Apple at the top of the set-top box market reflects several trends. Pay TV specific set-top boxes are becoming less important for consumers to access premium content, because Netflix, HBO Go and other OTT video platforms now offer top-tier content to retail OTT STBs.

“As retail STBs have grown in the market, traditional pay TV set-top vendors have been forced to re-position themselves, with significant consolidation at the top of the market, diversification toward software and services in the middle, and low-end vendors moving toward broader volume.”