After more than 40 years of operation, DTVE is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

Ovum: The rise of the TV re-intermediaries

The ongoing unbundling of pay TV by Netflix, Disney+, and other direct-to-consumer (D2C) video apps will undoubtedly be one of the defining trends of 2019. But the year will also see Apple, Amazon, Google, Roku, operators, and others seek to insert themselves between these apps and consumers in new and disruptive ways – with major implications for how TV is discovered, watched, and paid for.

The ongoing unbundling of pay TV by Netflix, Disney+, and other direct-to-consumer (D2C) video apps will undoubtedly be one of the defining trends of 2019. But the year will also see Apple, Amazon, Google, Roku, operators, and others seek to insert themselves between these apps and consumers in new and disruptive ways – with major implications for how TV is discovered, watched, and paid for.

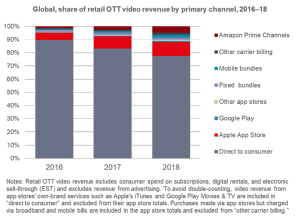

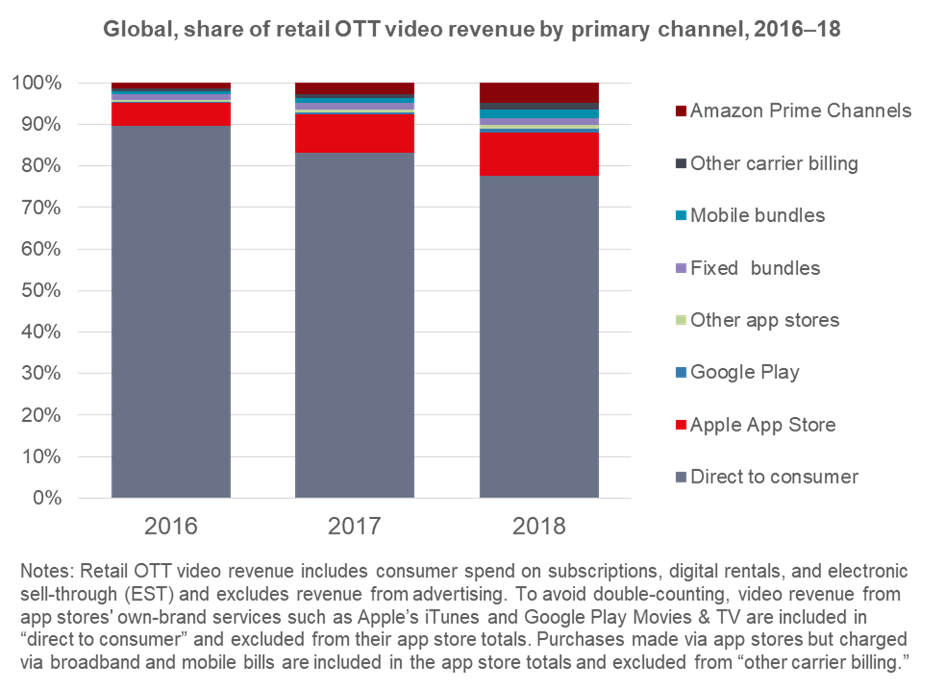

Ovum estimates that US$7.2 billion, or 22%, of total paid OTT video revenues flowed through such “re-intermediaries” in 2018 (see Figure 1). Consumers paid for UKS$3.9 billion of video rentals, downloads, and subscriptions via app stores and $2.1bn via telco bundles or their broadband or mobile bills, a mechanism known as carrier billing. A further US$1.6 billion of fees for D2C apps were billed via Amazon’s Prime Channels platform. Each re-intermediary took cuts of around 10–30% of these charges, equal to US$1.4 billion.

In 2019 and beyond, the TV re-intermediary market will expand beyond these key sources of revenue as Apple, Google, Amazon, Roku, and operators launch and evolve existing and new offerings around these strategies:

Winning customers: Taking the friction out of subscriptions. Ovum’s preliminary analysis suggests that by 2020, paid OTT video revenue billed through re-intermediaries will more than double to over US$16 billion, or 34% of the total, and their cut will approach £3.2 billion. Why? It’s more convenient for consumers’ increasingly smartphone- and app-centric lives. One major platform, for example, recently found that a significant number of customers continued to sign up via Apple’s App Store even after the provider increased fees by 30% for this option to offset Apple’s cut.

Winning customers: Taking the friction out of subscriptions. Ovum’s preliminary analysis suggests that by 2020, paid OTT video revenue billed through re-intermediaries will more than double to over US$16 billion, or 34% of the total, and their cut will approach £3.2 billion. Why? It’s more convenient for consumers’ increasingly smartphone- and app-centric lives. One major platform, for example, recently found that a significant number of customers continued to sign up via Apple’s App Store even after the provider increased fees by 30% for this option to offset Apple’s cut.- Content discovery: The new TV home screen. Historically, the placement of TV channels on pay-TV operators’ electronic program guides has had a major effect on their viewing figures. This influence will extend to the current and future TV re-intermediary plays of Amazon, Google, Apple, Roku, and others – but with an added twist. On “a la carte” platforms that allow users to pick and mix what they subscribe to, D2C apps may sink or swim depending on when and where they appear.

- Digital real estate: Pay to get played. The prominence of D2C apps will be determined partly by the re-intermediaries’ algorithms, but also by their commercial interests. More friendly partners might get preferential treatment, while direct competitors might be buried or rarely surfaced. Re-intermediaries already charge for placement, promotion, search, and concessions on revenue share deals. Only the most powerful brands will rise to the top without paying, especially as algorithms will remain a “black box” to outsiders.

- Video advertising: Cutting in on the value chain. Re-intermediaries will also seek to make money from video advertising within D2C apps. Late last year, Amazon told app providers on its Fire TV platform to hand over 30% of their ad space for its own use and use only its ad network to serve their own adverts. Such hybrid strategies will be critical to the tech giants growing their share of the US$180 billion-plus TV and video advertising market, combining their rich customer data with high-value TV shows, sports coverage, and other traditional content that many major brands still want their ads to appear next to.

- Bigger data: All-knowing, all-seeing, all-conquering? The role of re-intermediaries in providing a single place to search for, subscribe to, and watch TV will grant them a more unified view of consumers’ preferences, habits, and spending patterns than any single app. This data will not only offer powerful leverage in commercial negotiations with D2C providers, it could also fundamentally alter OTT video competition. Say an app, genre, or show suddenly shoots to popularity, a re-intermediary could quickly copy or buy it – just as they have in the traditional app world.

Netflix recently became the first app provider to publicly address the challenge of TV re-intermediaries, by dropping the ability of new users to sign up via Apple’s App Store. But it will probably be one of the few video apps powerful enough to convince people to subscribe independently and the tech giants to bend to its will; most consumers just don’t have time or interest to seek out and manage multiple video apps. For many D2C app providers, the future of TV might be less direct than they planned for.

Straight Talk is a weekly briefing from the desk of the Chief Research Officer. To receive this newsletter by email, please contact us.