After more than 40 years of operation, DTVE is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

DTVE Data Weekly: How the cloud and decline of broadcast are impacting video processing

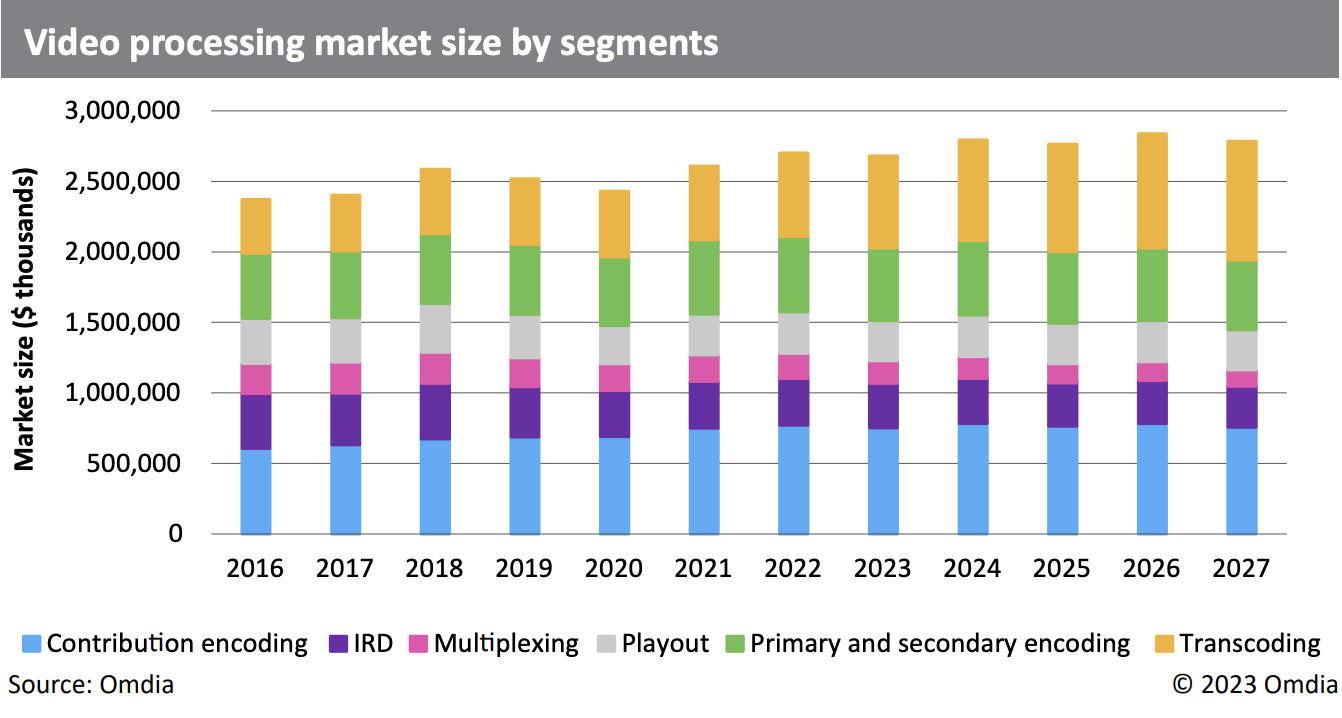

The video processing market grew by 7% in 2021 to US$2.6 billion, largely driven by growth in streaming technology in the overall workflow, such as transcoding, and a general rebound coming out of the most intense pandemic restrictions.

The video processing market grew by 7% in 2021 to US$2.6 billion, largely driven by growth in streaming technology in the overall workflow, such as transcoding, and a general rebound coming out of the most intense pandemic restrictions.

However, Omdia forecasts the broadcast-centric portion of the market to be in sustained decline by the end of the forecast period in 2027, as commoditization affects vendors’ ability to charge a premium for increasingly simplified and standardized OTT video processing.

Because of this, and as content budgets are often prioritized above technology budgets, video processing’s growth over the forecast term falls short of the revenue growth forecast for the television services its solutions enable. A decline in customers and income for broadcast services will affect the need for hardware encoders, IRDs, and multiplexers.

At a broader scale, alongside the longer-term reallocation of DTT and DTH spectrum, we must also recognize new standards and industry initiatives such as HbbTV and ATSC 3.0, which further blur the boundaries between traditional broadcast and OTT.

Video processing shifting to the cloud

The market is shifting to primary distribution via IP and the cloud. Broadly speaking, it will enable operators and service providers to reach more subscribers, reduce costs, and gain agility as video delivery requirements evolve to move increasingly large files and deal with ever-rising storage costs.

Operators and service providers are transitioning from traditional primary distribution networks to hybrid distribution frameworks that combine satellite and IP. Hybrid frameworks more easily integrate streaming operations, making for a managed transition, fostering video business growth, and reducing total cost of ownership. IP can cope with 4K, 8K, HDR, and a wider colour gamut, which is what broadcasters will need going forward.

Operators and service providers are transitioning from traditional primary distribution networks to hybrid distribution frameworks that combine satellite and IP. Hybrid frameworks more easily integrate streaming operations, making for a managed transition, fostering video business growth, and reducing total cost of ownership. IP can cope with 4K, 8K, HDR, and a wider colour gamut, which is what broadcasters will need going forward.

Although the widespread adoption of 8K is unlikely to be ubiquitous European power regulations inhibit the development of 8K – this may stay the conversion to full-IP workflows, and we might instead see IP “islands” in the chain typical of a hybrid approach.

New vendors are using the cloud to reduce prices, and service providers have less need to over-procure resources due to the cloud’s elastic capacity. The public cloud has built-in redundancy, so even adopting it as a backup for on-premises operations results in significant savings.

The issue for video processing vendors is to maintain margins by developing innovative services. For example, the core playout offering for broadcasters is not growing, but from a SaaS standpoint, certain playout vendors’ share of wallet will grow as commoditized hardware is phased out of the market in favor of efficient “channel-in-a-box” solutions.

The focus will be on solutions that reduce video service provider costs; as a result, bandwidth-saving technologies like context-aware compression and automated playout will increase demand for advanced solutions.

Thomas Thomson is senior analyst, media delivery at Omdia.

Omdia’s latest Video Processing & Playout Report is available here.