After more than 40 years of operation, DTVE is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

EU cable turns in record revenues despite TV decline

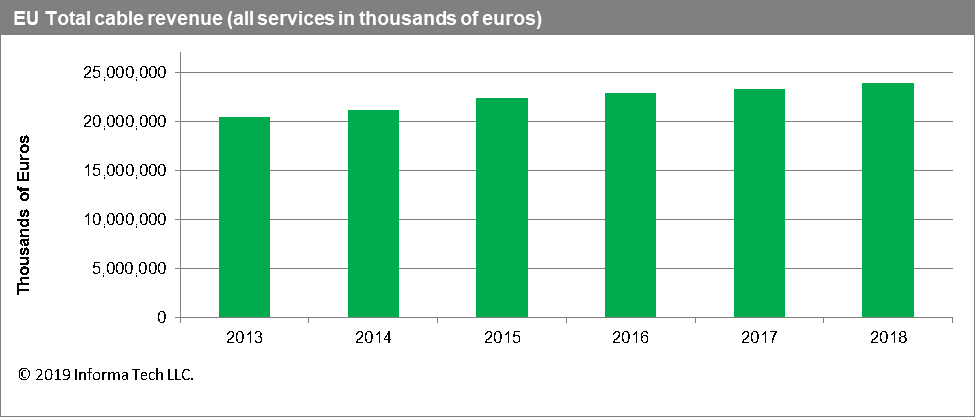

European Union cable market revenue rose to a record high of €24 billion euros in 2018, up 3% from €23.3 billion in 2017, according to data released by Cable Europe and IHS Markit | Technology, now a part of Informa Tech, publisher of Digital TV Europe.

The all-time-high revenue results were propelled by continued growth in the total number of cable revenue generating units (RGUs) in the EU, according to the European Broadband Cable Yearbook offered by Regional RGUs increased by about one million in 2018 to reach an annual high of 121.7 million, up from 120.6 million in 2017. The majority of the RGU growth originated from the broadband sector, where consumers are continuing to add subscriptions to cable internet services.

The all-time-high revenue results were propelled by continued growth in the total number of cable revenue generating units (RGUs) in the EU, according to the European Broadband Cable Yearbook offered by Regional RGUs increased by about one million in 2018 to reach an annual high of 121.7 million, up from 120.6 million in 2017. The majority of the RGU growth originated from the broadband sector, where consumers are continuing to add subscriptions to cable internet services.

Measured in terms of subscriptions, RGUs for cable internet service amounted to 38 million in 2018, up from 37.1 million in 2017. This growth helped drive the increase in overall EU RGUs for the year.

Internet RGU growth outperformed the other services offered by cable providers in the region. EU subscriptions to cable TV declined by 275,000 in 2018.

EU cable TV service subscribers, which increased for the first time in nine years in 2017, declined in 2018, falling by 275,000 homes to 55 million,.

Digital cable subscribers continued to rise in the region, increasing by four million to reach 45.2 million in 2018, as operators successfully converted significant numbers of subscribers from analogue TV to higher-value digital services.

Based on the power of bundled services, EU cable operators have grown total ARPUs by €9 over 10 years by selling more services.

Europeans still receive their pay TV via cable more than any other technology, despite the tough competitive environment.

Presenting the stats at Cable Congress, Maria Rua Aguete, executive director of media, service providers and platforms for IHS Markit | Technology, said that online channels are dominating video subscription growth in the US, with virtual pay TV failing to compensate for traditional pay TV’s decline. Pay TV subscribers in the US typically also take OTT TV services and use their traditional provider to access these services. Price is the main reason why US cable subscribers decided to churn.

In the rest of the world, however, pay TV has been more or less stable. Cable and satellite remain the main players, she said. Despite the lead of OTT in overall global subscription numbers, revenues remain dominated by traditional pay TV.

The picture in terms of cable TV additions and losses varies widely between European countries. Cable internet has also faced challenges, with fibre and telecom operators providing stiff competition, said Rua Aguete

Subscription TV is still rising, even if most of the additions come from online video services. Netflix accounts for 49% of all online subscriptions, followed by Amaxon with 20%.

The European cable market now has two main players – Vodafone and Liberty Global with 34% and 22% of the market respectively in terms of subscribers, she said. Other major players include RCS&RDS, Altice France and Tele Columbus.

Rua Aguete also said that Spain is the European leader in next-generation broadband access, coming after only South Korea globally. Some 50 European operators of all types meanwhile provide converged fixed and mobile services and a growing number of operators are launching 5G services.

Cable has also led partnerships with online video providers, particularly Netflix. “Cable has been the pioneer in this type of partnership,” said Rua Aguete.

Alternative routes for receiving premium TV are also on the rise. The market for smart TVs and smart speakers has expanded rapidly over the last year, the latter by 254%, while the smartphone market has grown modestly and the market for digital media adapters for TV has declined.