After more than 40 years of operation, DTVE is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

Why monetisation represents a growth opportunity for OVPs

Increasing sales via cloud marketplaces have generated significant demand for OTT deployments, streamlining the procurement of development tools and storage for broadcasters.

Other drivers include the rolling out of monetisation-as-a-service offerings as add-ons to the established OVP configuration and the steady migration of smaller service providers that do not have the in-house resources to procure streaming workflows.

Going forward, OVPs will increasingly be repositioned and reconfigured as modularised offerings. This is a key opportunity for them to grow their relevance with Tier 1 customers, leveraging their streaming nous to outmaneuver incumbent broadcast-centric suppliers, meaning that the OVPs will remain highly relevant as they redefine their role.

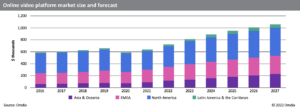

In this way, we see the OVP market expanding to US$1,059 million by 2027, an 8% CAGR from 2022. As advertising becomes a larger part of the monetization story for streaming service providers, OVPs are positioning themselves as key partners to optimise ad yields. Client and server-side ad insertion capabilities are a hallmark of OVPs rolling out monetisation-as-a-service offerings.

The CMS – the crown jewel product for leading OVP vendors – can configure the sponsored page, squeezeback ads, and dynamic product placement that adds extra layers of monetisation inside service provider apps for live and VOD content. Another innovation that some OVPs are employing is UX management – providing dashboards to content owners that allow them to adjust recommendation engines and configure layout types and menu design.

In this way, the app interface can be tailored to service provider specifications.

Because they tend to have less expansive product and IT teams, Tier 2 and 3 service providers are likely to work with fewer vendors. Tier 1 clients are more likely to be more particular with workflow components as they have the resources to handle greater complexity.

In certain regions – Asia & Oceania and Latin America being strong examples – service providers are more likely to have hybrid or entirely on-premises solutions due to lower public cloud infrastructure and services penetration in these regions.

Ad monetisation-as-a-service

The pivot of OVPs toward ad monetisation-as-a-service solutions by catering to FAST-hungry service providers will be challenged by TV operating systems with owned and operated ad platforms. Large TV OEMs that run their own OS, such as Samsung, are vertically integrating their ad stack and forcing publishers to work with them on content delivery and SSAI, meaning it is becoming more of a black box for content publishers.

This presents a challenge to the likes of Brightcove and JWPlayer, which increasingly play in the advertising space. TV operating systems will want to capitalise on that ad spend and diminish third-party involvement in content and ad delivery, diverting ad demand away from OVPs.

Thomas Thomson is senior analyst, video technology at Omdia. For more on this topic, click here.