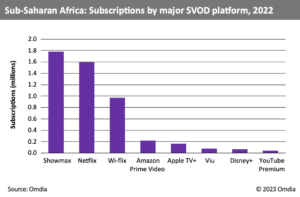

African OTT: Wi-Flix’s challenge to Showmax and Netflix

OTT video adoption in sub-Saharan Africa continues to grow at an impressive rate, with subscriptions reaching almost 4.5m and revenue growing to $294m in 2022. Showmax and Netflix are the region’s standout market leaders for now, but Omdia is monitoring some new fast-growing players, such as Wi-flix, which are looking to capture their own share of the African streaming opportunity.

OTT video subscription penetration in sub-Saharan Africa reached 5.7% in 2022. As mobile and fixed internet connectivity improves, smartphone adoption is increasing, and OTT operators continue to adapt their offerings to mobile-first markets through initiatives such as mobile-only subscription tiers. Omdia forecasts online video revenue in the region to increase at a CAGR of 9.6% from $294m in 2022 to $510m by 2028.

Wi-flix has experienced considerable growth in the past few years, with an active customer base of 972,000 paying subscribers, with 90% based in sub- Saharan Africa and 10% coming from the diaspora. Subscription revenue grew by over one thousand percent between 2021 and 2022, with the company claiming a paid customer retention rate of 75%.

Content strategy is critical, as shown by its major competitors. In sports, Showmax has a competitive advantage: because it is a subsidiary of MultiChoice Group, its Showmax Pro and Showmax Pro Mobile subscribers gain access to premium live sports from MultiChoice-owned sports channel SuperSport.

Meanwhile, Netflix has been investing heavily in local sub-Saharan African content acquisition and production, with major successes such as the South African series Blood and Water, released in 2020. Local content is king in Africa, and Netflix has already invested over €160m ($176m) into film content production since launching in the region in 2016. Wi- flix is also looking to move beyond content acquisition and partnerships, with plans to set up a production entity in Ghana soon. The company also has three Wi- flix originals currently in post-production. Although Wi-flix will be unable to go head-to-head with Netflix on production budgets, this strategy could serve as a differentiator against smaller OTT platforms in the region by providing subscribers with lower-cost proprietary local content, given the strong appetite for homegrown original content.

Meanwhile, Netflix has been investing heavily in local sub-Saharan African content acquisition and production, with major successes such as the South African series Blood and Water, released in 2020. Local content is king in Africa, and Netflix has already invested over €160m ($176m) into film content production since launching in the region in 2016. Wi- flix is also looking to move beyond content acquisition and partnerships, with plans to set up a production entity in Ghana soon. The company also has three Wi- flix originals currently in post-production. Although Wi-flix will be unable to go head-to-head with Netflix on production budgets, this strategy could serve as a differentiator against smaller OTT platforms in the region by providing subscribers with lower-cost proprietary local content, given the strong appetite for homegrown original content.

Local content

Wi-flix has over 30,000 hours of content and 10 live streaming channels available on its platform. Importantly, around 70% of its content is local, with the remaining 30% from international sources. The streaming platform has adopted a collaboration strategy, signing up with over 200 content partners with which it has structured revenue share agreements; Omdia sees this as a key way for smaller OTT players to expand their catalogs cost-effectively.

Telco partnerships have been a critical component of Wi-flix’s growth strategy, as they provide carrier billing solutions and subsidized data costs for subscribers. Wi-flix is negotiating an integration deal with Safaricom to launch full operations in Kenya in 2024, following a soft launch in 2020. Wi-flix also has a channel on MTN-owned free super-app Ayoba, with 300,000 subscribers, which has acted as a marketing funnel for paid subscribers to Wi-flix. Despite revenue share agreements being in place, telco partnerships in the region serve primarily as a conduit for payment facilitation rather than as channels for OTT video customer acquisition. As a result, startups like Wi-flix will still require large marketing and distribution budgets to compete with Netflix and Showmax, which have much stronger balance sheets. There is still some way to go before the likes of Showmax and Netflix need to worry about Wi-flix and others like it.

Samuel Nkwam is a research analyst, TV & online video at Omdia.