After more than 40 years of operation, DTVE is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

DTVE Data Weekly: Nordic TV markets

Source: Omdia

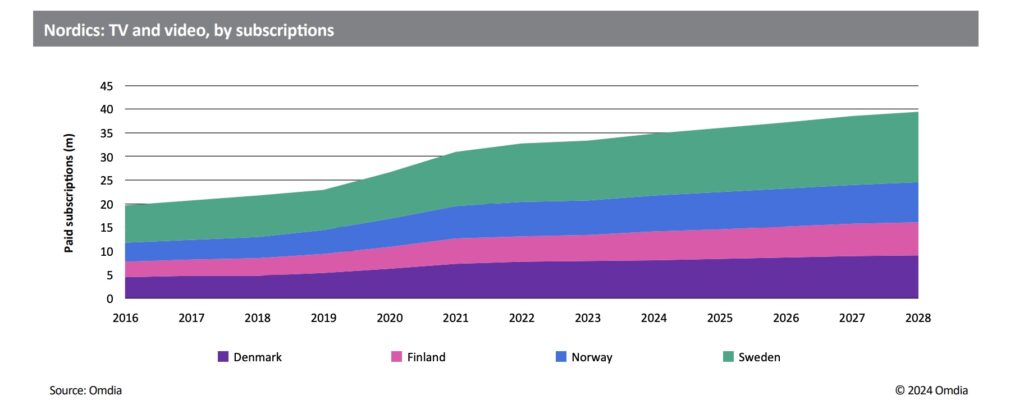

The Nordic market remains mature for TV and video, and all signs post-COVID-19 suggest stability in Nordic TV buying and viewing habits. Nordic pay TV is coming out of a period of consolidation that has seen multiple key services being rebranded and remarketed. As part of this, there have been sharp declines in cable TV subscriber numbers, allowing IPTV to grow to become a key pay-TV sector.

Omdia does not anticipate any significant changes to present pay TV and streaming market shares over the foreseeable future. For pay TV, consolidation is now in the past, and current market leaders are expected to refocus on maintaining market shares. At the same time, the landscape for online video streaming is largely set; Omdia does not expect any significant new entrants in the SVOD sector.

The Nordic region was a very swift adopter of online video streaming. There was previously widespread dissatisfaction with the available pay-TV options, and the public was, therefore, prepared to pay significant fees to adopt online video alternatives as soon as they became available.

Pay TV vs Online Video offerings

To illustrate this change, Omdia has compared the price of traditional pay-TV ARPU to a pay-TV-like package of online video services that customers can create as a self-bundled alternative to pay TV. This theoretical self-service bundle comprises the top three generalist streaming services (Netflix, Viaplay, and HBO Max) plus a subscription to two add-on specialist sports streamers (Eurosport Player and DAZN).

The aggressive demand for online video content— and willingness to pay for it—is highlighted by the fact that, as long ago as 2016, the cost of creating such a streaming bundle ($43.35) was already 1.56 times higher than the cost of the regional pay-TV ARPU ($27.70). By comparison, in the US, the price of a similar online video bundle is still significantly behind the cost of traditional pay TV, and Omdia’s data shows that the US “bundle” price is not expected to catch up with pay TV until 2028.

The trend shown by the regional Nordic data is replicated, by and large, in Denmark, Finland, and Sweden. Norway is somewhat of an outlier with its historically higher pay-TV pricing, meaning that the selfbundle pricing remains below the average cost of pay TV. However, that is changing, and the bundle cost will overtake the cost of pay TV over the next few years.

All four Nordic markets have strong public broadcasters, which are non-commercial. They have all replaced the license fee with public service taxes (with Norway most recently doing so in 2019). Nordic broadcasters are in a strong position to retain their popularity despite declines in TV advertising revenue. Broadcasters’ existing relationships with big brand advertisers and local agencies mean they will remain central to ad-based content monetization for the foreseeable future.

There has been some concentration in commercial TV and pay TV: Telia owns TV4 in Sweden and MTV in Finland. In Norway, TV2, owned by the Egmont Group, has become a leading player in pay TV as well as FTA. Current market leaders for pay TV—and, by extension, the existing Nordic virtual or online pay-TV services such as Viaplay—are crucially dependent on key sports rights to retain existing subscriptions.

Similarly, Warner Bros. Discovery remains a significant player in sports: it owns the rights to the Danish and Swedish football leagues and the Olympics to 2032. It will cede rights to the Danish league to TV2 from 2024.

TV advertising revenue is in secular decline in the Nordics, driven by a strong shift of TV viewing toward streaming. This is exaggerated by a relatively weak broadcaster VOD advertising segment, which is due to broadcasters historically prioritizing subscription models over advertising for online video monetization. In addition, the region has a weak macroeconomic environment, which is widely expected to improve after 2024. Omdia anticipates TV advertising revenue to be in overall decline through 2028.

A weak macroeconomic environment and consumer shifts to online viewing have led to a substantial decline in linear TV ad revenue in the Nordics. This is not offset by strong growth in broadcaster VOD ad revenue, itself hampered by broadcasters favoring subscription-based online video monetization in the Nordics. There are signs from the likes of Viaplay that this strategy will change, but Omdia still expects Nordic TV broadcaster ad revenue to fall by $49m from 2023 to 2028.

Source: Omdia

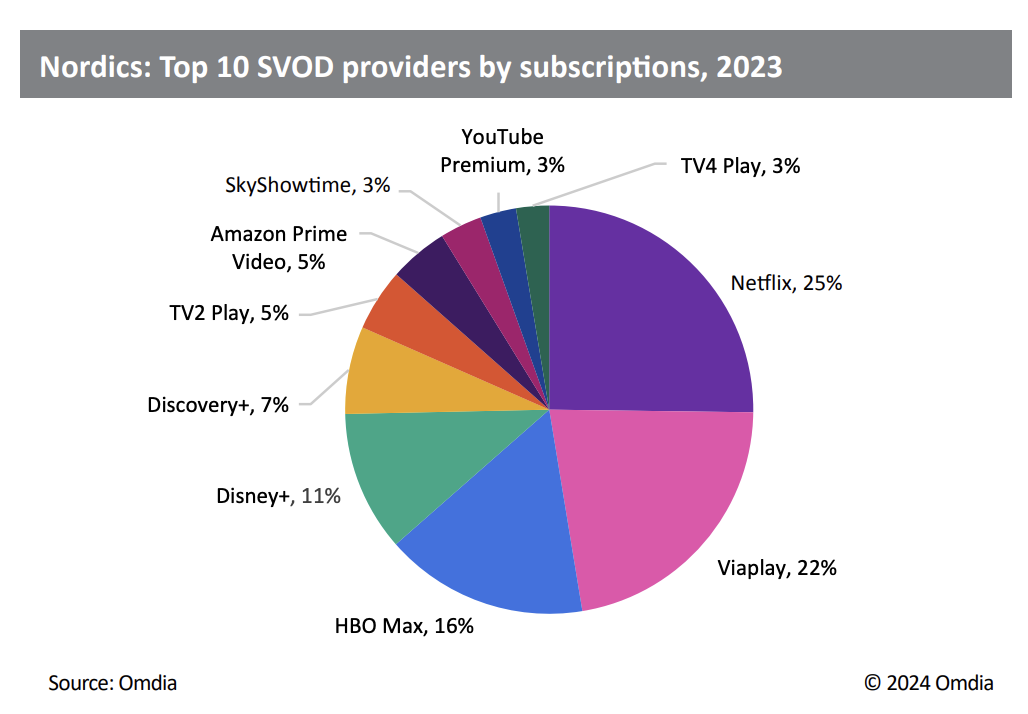

The arrival of multiple new SVOD services after 2020, including Disney+, Amazon Prime Video, and SkyShowtime, has greatly increased the market for SVOD in the Nordics, directly eating into an established market for pay TV. The US major services generally dominate, but each of the four Nordic countries has 1–2 local streaming services in the top five ranked SVOD.

The level of growth for SVOD is now significantly decelerating, and for the first time ever, SVOD is at single-digit annual growth rates. In turn, a multiyear contraction of pay TV is showing signs of decelerating. As a result, Omdia does not anticipate that the current market shares for pay TV or SVOD will significantly change for the foreseeable future.

Viaplay’s future

Despite the well-publicised turmoil for Nordic incumbent pay-TV and streaming company Viaplay in 2023, Omdia believes that Viaplay is too big to fail, particularly in its domestic Nordic markets, where it continues to hold significant market share. The sudden decline in subscription numbers in 2023 was its first real test, causing a major upset to investors and forcing through a major restructuring of the company. It is now looking to refocus on its domestic Nordic markets instead of chasing wider ambitions to become the largest European streaming service.

As part of this change, Viaplay has already increased its prices across the board, and it is explicitly moving away from what it calls “low-ARPU” bundling telco partnerships. Omdia believes the investment in Viaplay by Canal+ will potentially offer more financial stability (and additional know-how in pay TV).

Separately, Viaplay has recently acknowledged in the media that it may have to move toward an advertising-supported subscription model. With its experience operating ViaFree, its dedicated AVOD platform (which merged with Paramount’s Pluto TV in the Nordics last year), Viaplay is in a good position to capitalize on its existing in-house ad tech and relationship with Nordic advertisers. Paramount’s approach of partnering with Viaplay for distribution and ad sales of Pluto TV in the Nordics is a testament to the continued strength of broadcasters in the ad market despite revenue declines.

From 2024, most streaming services in the Nordics will shift business models from pure pay models to hybrid subscriptions with advertising. The impact is likely to be a short-term uptick in streaming service subscriber numbers as customers take advantage of cheaper services, but the longer-term impact may be greater seasonality and churn for streaming services. In an uncertain Nordic TV advertising market, hybrid ad tiers are unlikely to greatly bolster SVOD revenue in the mid-term.

Tony Gunnarsson, is Omdia’s principal analyst, TV, video & advertising