YouTube dominance, SVOD decline and pubcaster strength: key takeaways from Ofcom’s Media Nations 2022 report

It is that time of year where UK broadcast regulator Ofcom publishes its Media Nations report, and the headline story is a record generational divide between the younger Brits raised on streaming and the old-habits-die-hard older population still propping up traditional linear TV.

According to the eagerly anticipated annual report, people aged 16-24 spend 53 minutes in front of broadcast TV on an average day, down 66% over the past decade. Adults aged over 65 by contrast spend an average of 5 hours and 50 minutes per day watching broadcast TV, slightly higher than 10 years ago.

While nine in ten 18-24-year-olds typically bypass TV channels and head straight to streaming when looking for something to watch, 59% of 55-64-year-olds and 76% of those aged 65+ still turn to TV channels first.

But while this dichotomy is one which has dominated discussions surrounding the report, there are plenty of other aspects of this inquiry into UK video consumption worth examining more closely.

YouTube, not Netflix or Disney, is the dominant force in video streaming

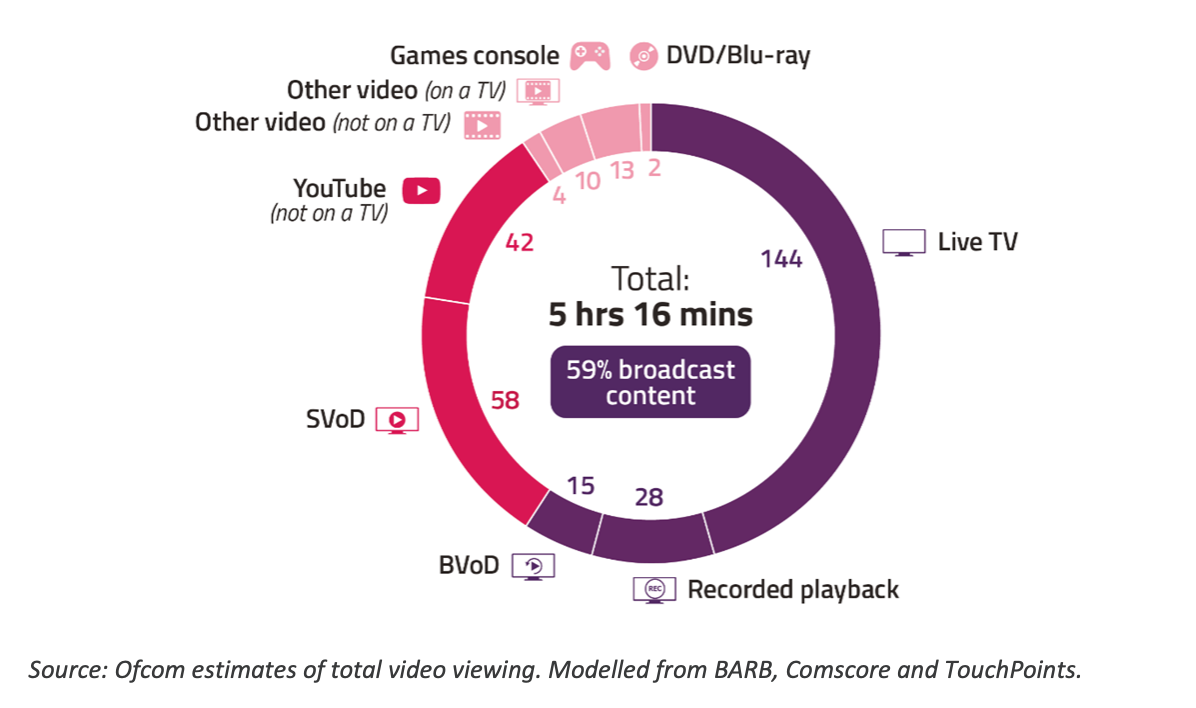

Skimming through the report there is one graphic which stands out most to me. It appears on page five and outlines the average minutes of viewing per day across all individuals on all devices.

The average brit spends 5 hours and 16 minutes per day consuming video. Of that total, 59% of it is broadcast content; 144 minutes on live TV, 28 minutes on recorded playback and 15 minutes on BVOD.

Average minutes of viewing per day, all individuals, all devices

While much has been made of the startling difference in consumption habits as detailed above, that 16-24 age category is still a small part of the population by comparison to people raised on a diet of the BBC and, in wealthier households, Sky, Virgin Media, NTL or whatever was the pay TV offering du jour at the time.

There is next to no chance that the broadcast content percentage will ever be this high again, and it may drop to under half within the next decade. It was at 61% in 2021, 59% in 2020 (but worth bearing in mind that this was at the height of the Covid-19 pandemic when streamers gained a huge advantage with a constant flow of fresh content), and 71% for the first report in 2018. (The 2019 report only produced a comparable chart for 16-34-year-olds).

The remaining 41% of the average Brit’s video time is dedicated to streaming, though within that there is only one specific platform mentioned by name: YouTube.

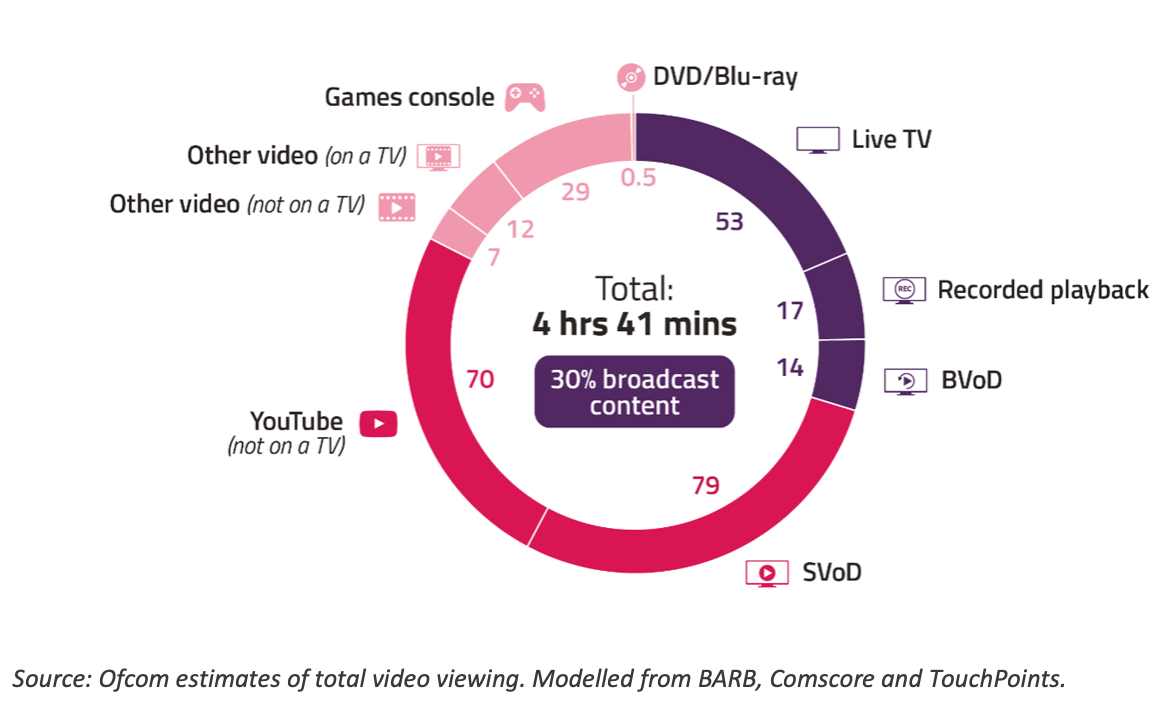

Average minutes of viewing per day, all aged 16-34, all devices

Of course, YouTube’s average of 42 minutes per day is much smaller than SVOD’s 58 minutes per day, but that is across the wide range of subscription streamers which themselves have struggled this year (more on that later). The total is much higher for people aged 16-34, who watch an average of 70 minutes per day on YouTube, while SVOD is at 79 minutes per day.

But consider for a second that Brits are, on average as a country, spending almost three-quarters of an hour per day specifically on Google’s video platform and specifically consuming that content away from a television screen. It’s no wonder that YouTube is looking to join the likes of Amazon, Apple and Roku by getting into service aggregation.

This translates to the UK alone spending 4.7 billion hours per day on YouTube, consuming everything from last night’s football highlights and news coverage to music videos, kids content and, yes, funny cat compilations. That’s an hour for every dollar Google spent to acquire YouTube in 2006 – and that would get you to just before 5am.

So it’s clear the constant subscriber size comparison contest with which global streaming giants seem obsessed, it is YouTube, not Netflix, Amazon nor Disney that is by far the dominant force in video streaming in the UK.

SVOD decline and cost-of-living

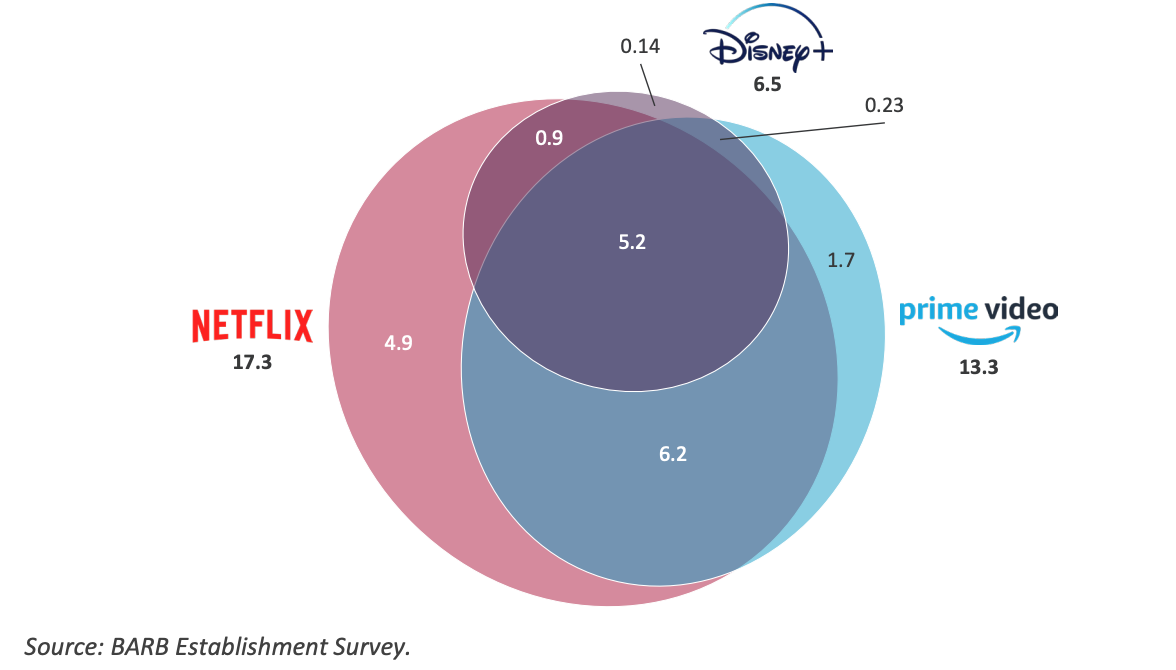

This is not to say that the trio of streamers are struggling by any means. A fifth of UK homes (5.2 million) subscribe to all three platforms, at a cost of around £300 per year per household. To once again do the sums, means consumers in the UK are spending roughly £2.02 billion per year on Netflix, Prime Video and Disney+ – and that’s just from households with all three. The real total from across the entire country from each of these services is astronomically higher.

Households subscribing to one or more of Netflix, Amazon Prime Video and Disney+, and overlaps between them (millions): Q1 2022

SVOD services broadly, including the big three, were used by 67% of UK households in Q2 2022, marking a slight decline from a peak of 68% in Q1.

The report’s executive summary however points out that “the number of households yet to try SVoD is becoming smaller and harder to convert, resulting in slower subscriber growth,” while the looming impacts of the cost-of-living crisis – a crisis which could send two-thirds of UK families into fuel poverty – “is is making customer retention more challenging.”

The impact of the cost-of-living crisis on video spend in the UK is something I explored in one of these columns earlier this summer, but the main point to get across is that, despite presenting extraordinary value when compared to physical media of old, consumers are re-evaluating their outgoings and the flexibility afforded by no contract SVODs and the abundance of free, ad-supported television (FAST) services available puts that high subscriber count at risk.

The report provides quotes from a number of Brits who describe SVODs as a “waste of money”, or that they “could not afford to keep [Netflix] going”. In its survey, 2% of Netflix users had cancelled their subscription in the past three months, with 4% of both Prime and Disney+ subscribers doing the same. Smaller SVODs had a cancellation rate of up to 16%, with cost cited by 36% of all respondents as a reason for either trimming down their number of subscribed to services or cutting them out altogether.

In total, SVOD subscriptions fell by more than 350,000 in spring 2022 to 19.2 million, though three-quarters said they would resubscribe depending on changes in programmes, needs or circumstances.

In total, SVOD subscriptions fell by more than 350,000 in spring 2022 to 19.2 million, though three-quarters said they would resubscribe depending on changes in programmes, needs or circumstances.

Both Netflix and Disney are introducing ad-supported tiers in the US in the coming months. But those companies – along with the likes of Paramount+ which launched here without an ad-supported option despite offering it elsewhere – would be wise to expedite any plans to introduce them in the UK at a time when the ‘zombie government’ is providing little confidence that it will support low income families through the recession.

Pubcasters demonstrating their value

Speaking of the government, from day one of Boris Johnson’s soon-to-end tenure as prime minister of the UK he launched an attack on the BBC’s funding model and made no secret of wanting to abolish the licence fee as quickly as possible and with prejudice. Johnson’s government finally made the call to stamp out the licence fee from 2027 (with no proposed alternative funding model) earlier this year, but this would undoubtedly have come much sooner into his premiership were it not for that pesky pandemic. (Coincidentally, the BBC News Special on January 4, 2021 where the PM announced the country’s return to lockdown was the tenth-most watched programme of the year, the report shows.)

At the same time, culture secretary Nadine Dorries has made it her mission to privatise Channel 4 (despite displaying her ignorance of where its funding comes from in parliament). The MP also has made no secret of her disdain for the broadcaster, alleging that a reality TV show she appeared on featured paid actors in the place of the west London family with which she was staying. For its part, Channel 4 and Love Productions both provided evidence to the contrary of Dorries’ claim.

ITV is yet to be targeted by the Tories, but they probably know that messing with the home of Love Island would do worse for them in the polls than staging a poorly-judged Christmas quiz.

What’s clear is that the Conservative government has not created a particularly positive relationship between it and the media which it has a stake in, but Ofcom’s report shows that hasn’t stopped Brits from being satisfied with their services and content.

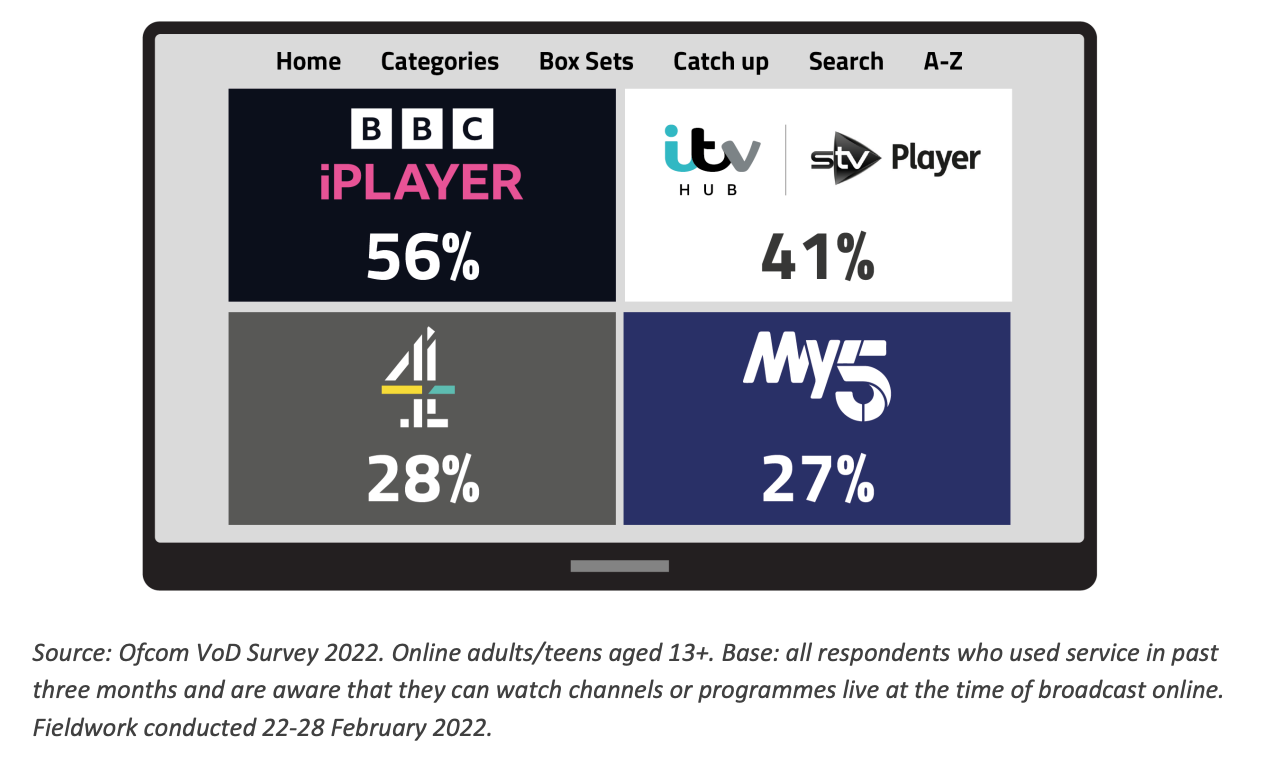

Proportion of online adults and teens who watch channels or programmes at the time of broadcast on BVOD services

Almost a third of the report is dedicated to public service broadcasting, but the main takeaway in this regard is that there is “broad satisfaction with public service broadcasting among those who watch it.”

A little more than two-thirds of PSB audience (67%) said they were satisfied by PSBs over the first half of 2022, while only 12% said they were dissatisfied. Crucially at a time when misinformation is rampant across social media and the wider internet (I’m looking at you, YouTube), PSBs are viewed as a trusted source of accurate UK news.

PSBs have seen audiences and levels of viewing continuing to fall, with the weekly reach of PSB channels falling to 76% of all individuals (down from 80% in 2019), while only 47% of 16-24-year-olds watch at least 15 minutes of PSB channels in an average week.

But while the traditional PSB linear channels may not be consumed by younger generations, the use of BVOD services has seen a significant increase. Some 82% of Brits said they’ve used a player like ITV Hub or BBC iPlayer in the past six months. Six in ten said they use these platforms to watch content live, while the average time spent watching services such as BBC iPlayer, ITV Hub and All 4 increased to 15 minutes per day, up by three minutes per person per day.

The report goes into more detail here, arguing that “VOD services are central to the PSBs’ strategies and are critical to driving future viewing and revenue”. It notes that though the increase in BVOD consumption does not make up for the losses in linear viewing, products like ITVX and strategic partnerships such as the one between Channel 4 and YouTube will further accelerate digital growth and develop new revenue streams.

In summary

Overall, Ofcom’s Media Nations 2022 report paints a picture of a UK that is in change. There is a clear generational divide both in terms of how Brits want to watch video, but also where they want to get it from.

Concerns of cost are increasingly impacting the once stable growth market of SVOD, and users are seeking alternative options which either offer content for free in exchange for advertising or at a discounted price.

But while there is a lot of change, the reliable institutions of PSBs are continuing to provide Brits with stability and a reliable source of entertainment and information, even if they’re doing it away from the traditional means. I would not be so trite as to argue a cliche like ‘the more things change, the more they stay the same,’ but there is undoubtedly comfort provided by these historical mainstays which should ensure support from the public even as the government attempts to dismantle them.

The 2023 report will surely give us a bleaker outlook as the cost-of-living crisis engulfs the country, but for now at least there is some room for reserved optimism.