DTVE Data Weekly: Streaming in North America

Source: Omdia

Omdia’s Pay TV & Online Video Report North America – 2023 looks at the region’s latest full-year data for 2022 and has found that direct-to-consumer services in North America have grown significantly in 2021 and 2022. With so many “must-have” streaming services saturating the market, consumers began exhibiting “churn and return” behaviour, where users subscribe in and out of streaming services depending on content release schedules.

In tandem with consumer self-bundling, corporate owners realized that saturation of services potentially limits subscription uptake and began consolidating. This came in the form of online channel mergers, acquisitions, and bundling.

In addition, hybrid tiers and online linear TV (FAST channels and simulcasts) became more widely available on device platforms, SVOD services, and premium AVOD services throughout 2022.

While 2020 and 2021 saw the creation of PVOD and PEST windows and high-value content going straight to owned-and-operated streaming services, studios and licensors pushed windows back to more pre-pandemic windowing strategies in 2022. With normalcy returning across windows, higher revenue can be earned at the title level.

In 2022, inflation fears and a cost-of-living crisis set in across global markets. Pressures on discretional consumer spending grew, and saturated services like Netflix and Disney+ saw some quarters of stagnant subscription growth. Cord-cutting also accelerated as consumers continued to weigh the value of pay TV against self-bundling streaming services.

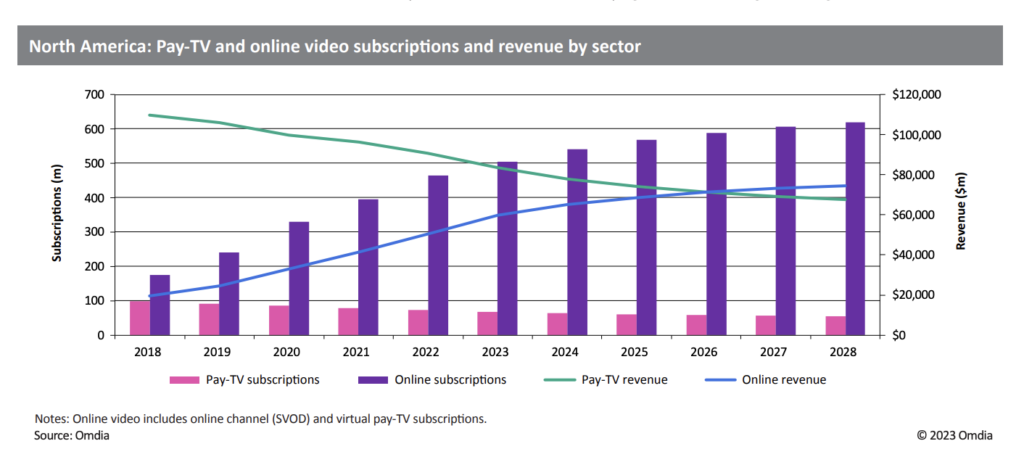

Omdia now expects online subscription revenue to eclipse North American pay-TV revenue in 2026. Annual pay-TV subscriptions experienced their steepest declines in 2022, further accelerating cordcutting. With increased subscription growth and higher cord-cutting, we now expect online channel revenue to eclipse pay-TV revenue for the first time in 2026.

Source: Omdia

Although online video households surpassed pay-TV households back in 2018, pay-TV ARPUs are 10x higher than online video ARPUs. More subscriptions per household, cord-cutting, and higher online video ARPUs drive this convergence.

Live sports and news content keep consumers tied to pay-TV subscriptions. US consumers are opting for virtual pay-TV subscriptions more often for live sports content because packages can be cheaper than traditional pay TV, and they can be shared across multiple households.

As pay-TV subscriptions decline, telcos are shifting their focus toward aggregation, bundling, and broadband connectivity. Consumers are looking for aggregation solutions to make billing management and content discovery easier. Device and smart TV operators are also vying to own the end-to-end consumer relationships.

In 2022, online subscription revenue reached $50.6bn, and pay-TV revenue hit $90.8bn. Despite fighting churn and subscription stagnation, Netflix’s subscription revenue grew by 8% in 2022, and it remains the largest SVOD operator in the region.

The North American streaming market

FAST channels generated just over $4bn in ad revenue in 2022. The growth of connected TV drives this market and is building out a linear TV experience online similar to that of the traditional pay-TV experience. Native AVOD and SVOD services are integrating FAST channels into their offerings.

In the US in 2022, the average inflation rate was 8%. Rising costs of living are forcing consumers to make spending trade-offs and encourage churn-and-return behavior. Despite inflationary pressures, the SVOD market grew in 2022; however, the rate of service stacking grew, and more consumers began turning to free ad-supported offerings.

As new SVOD services quickly grew in adoption and popularity in the US market, consumers have been faced with juggling over 10 “must-have” streaming services. From 2021 to 2022, churn-and-return behavior has only intensified with higher streaming costs and inflationary pressures. Increased churning has also encouraged services to lean more heavily into aggregation and bundling opportunities because these reduce churn.

Consolidation has increased significantly in 2022 and 2023. It allows services to grow their pipelines of original content and prove the value of increased pricing to consumers. Consolidation benefits consumers if it allows price flexibility with AVOD tiering or decreases the quantity of “must-have” services in the market. Too much consolidation, however, may decrease market competition, raise pricing too much, and therefore push consumers away.

Source: Omdia

Corporate owners lean into service consolidation versus disparate service offerings.

- Paramount+ with Showtime launched in the US in June 2023, and the Showtime standalone OTT service will close by the end of 2023. The integration will come with a price increase and more content for the Paramount+ service. ViacomCBS also rebranded to Paramount at the corporate level.

- The combined Hulu and Disney+ offering joined the market at the end of 2023. Integrating the services into one app experience will discourage consumers from leaving the Disney-owned app and likely increase viewing.

- The merger between Warner Bros. and Discovery was one of the first dominoes that started streaming service consolidation in the US. Prior to this merger, services—especially Disney—leaned into the portfolio approach. WarnerBros. Discovery also shuttered the early streaming services from CNN+ once the corporate merger was complete.

- After Televisa and Univision completed their merger in January 2022, the company focused on rolling out a holistic Spanish language streaming service, Vix and Vix+. Pantaya was an optimal acquisition target with an established Hispanic consumer base in the US.

Sports OTT services

League-owned streaming services and OTT sports licensing deals have become more popular in recent years. There were 34.4m subscriptions across sports specific OTT services in the US at the end of 2022. When including virtual pay-TV operators and general audience streaming services with access to sports content, 219.7m subscriptions had access to sports in 2022.

In 2022, Amazon Prime Video hosted the exclusive rights, across linear and OTT, to the NFL’s Thursday Night Football games for the first time. YouTube also acquired the rights to NFL Sunday Ticket, which will be shifting from DirecTV for the 2023 season. Apple secured exclusive rights to the MLS and packaged it in its suite of services.

Blackouts and national licensing deals complicate local consumers’ ability to watch live games without a pay-TV subscription. As more consumer viewership shifts to OTT and advertisers gain confidence in online CPMs, more licensing shifts will occur over the next five years.

Linear simulcasts and FAST channels may be an online opportunity for sports access on hybrid services.

Online video revenue grows

In 2022, online subscription revenue reached $39.2bn in North America.

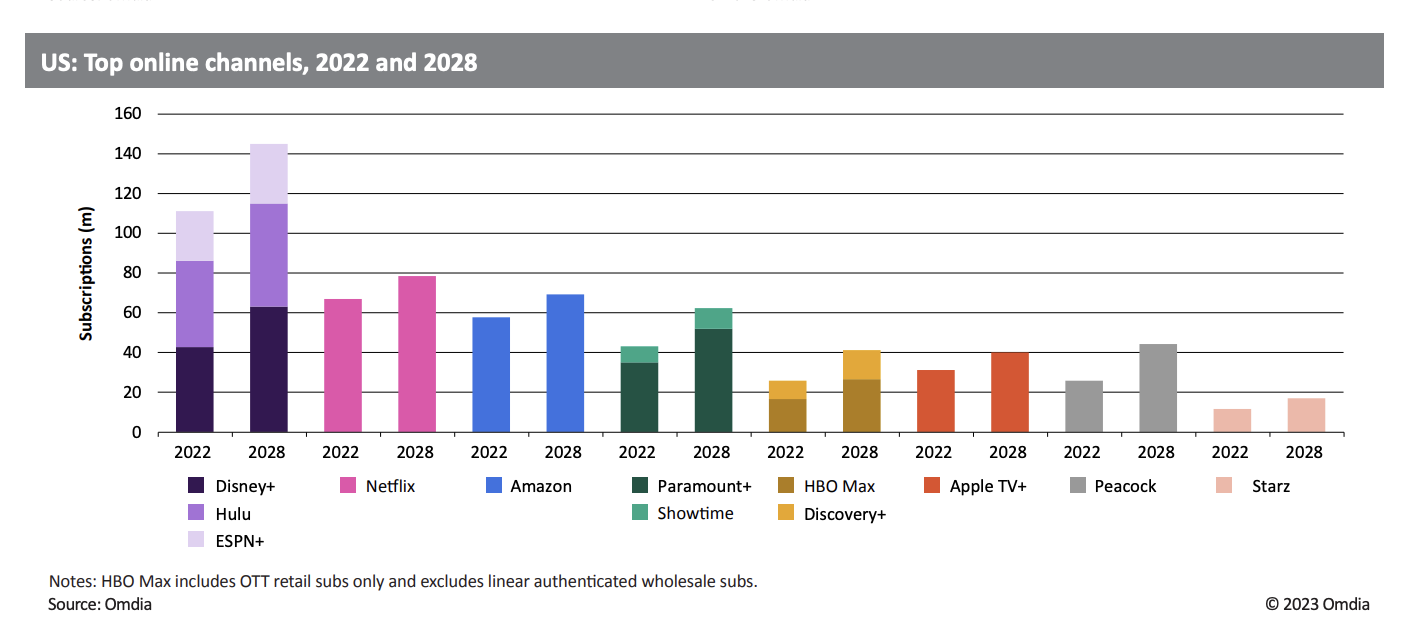

Netflix dominates online channel revenue in the US, accounting for 36% of total 2022 consumer spending in the region; this is down from 41% of the total in 2021. Although Netflix is losing share, its annual revenue continues to grow and increased by $1.1 bn from 2021. Netflix’s subscription revenue is about 4x higher than Disney+, which holds the second-highest spot.

The top five streaming services all lost share year over year due to the impressive growth of services across the board. Netflix revenue was followed by Disney+ (9%), Hulu (8%), and HBO Max (7%), which was the fourth-largest channel by revenue. HBO Max surpassed Amazon Prime Video in 2022, moving up in share.

Sarah Henschel is Omdia’s Principal Analyst, Media & Entertainment