DTVE Data Weekly: Turkish TV & video 2023 performance

Source: Omdia

Turkey’s pay-TV and online video markets have faced substantial challenges over the past five years, including poor rural connectivity and a deadly earthquake in 2023. Many of these challenges have been compounded by several years of rampant inflation. In the face of such substantial challenges, Turkey’s market has shown significant resilience: pay-TV subscription numbers are generally growing, and online video subscriptions continue to increase.

This resilience has been supported by two key pillars: a continued pipeline of high-quality content, which is now being exported globally, and the patience of providers, which have shown a willingness to delay price increases in the short term in the hope of recouping ARPU over the long term. As this pricing challenge gathers pace, the need for the right content, platforms, and packages has never been greater. Omdia’s analysis looks at each major OTT and pay-TV operator with the aim of highlighting key strategic priorities for each.

Linear TV

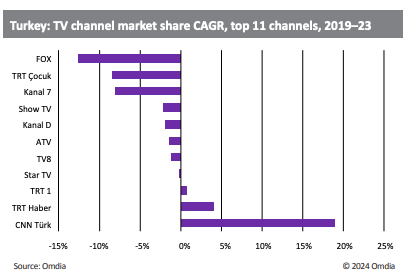

Turkey’s linear TV channel landscape is changing, but these changes are taking place slowly. Major general entertainment broadcasters such as ATV, Kanal D, and Show TV continue to dominate ratings, and although their audience shares are dropping by 1–2 percentage points a year, they continue to hold most of their audience. The decline of linear TV in Turkey is, therefore, happening slowly. In general, the market share of the 11 leading channels has consistently decreased. In 2019, these channels accounted for 62% of all viewing, but by 2023, this had fallen to 55% of the market as viewers watch an increasingly diverse range of channels and peak audiences fall. These declines in viewership are seen in prime time and across income brackets. Children’s channels are experiencing the most consistent viewership declines in Turkey, and news channels experienced the biggest increases in the 2023 election year.

Turkey’s online video market has seen many of its main providers alter their strategies. Amazon’s position in the e-commerce market in Turkey is nonmonopolistic, with strong competition from local rival Hepsiburada, so Amazon Prime Video has been forced to maintain competitive pricing to compete in e-commerce. Hepsiburada has a premium bundle that includes BluTV, Turkey’s first flagship domestic OTT platform. The Hepsiburada premium bundle launched in 2022 and by late 2023 had reached 1.3m subscriptions, of which around 70% are believed to be active users of BluTV.

Other platforms, meanwhile, have altered their strategies in terms of content. Acun Ilicali’s Exxen launched in September 2020. The initial focus of the platform was a mix of programming not seen usually on traditional Turkish TV, such as offbeat comedies and comedy talk shows using online talent. In June 2021, Exxen acquired streaming rights to three seasons of the UEFA Champions League and has since become a highcost operator.

Meanwhile, unlike some other international players, Netflix has consistently invested in Turkish content with, for example, the third series of the hit show The Tailor, released in late 2023. Amazon, meanwhile, launched its first Turkish series and movies in 2023. Disney+’s approach has contrasted with that of other providers; to rapidly grow its audience in Turkey, Disney+ acquired the rights to several popular franchises at launch; in 2023, many of these franchises were cast off as part of costcutting measures. The diversity of these approaches underlines the relative uncertainty in Turkey’s online video market.

Source: Omdia

Pay TV

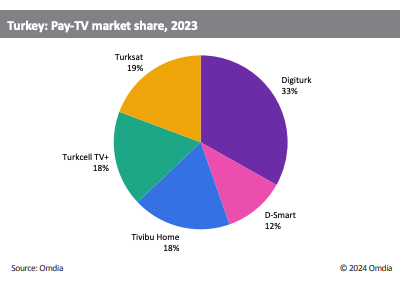

At the end of 2023, Turkey had 7.6m pay-TV subscriptions. Pay-TV penetration in the country is relatively high as a result of the slow rollout of free DTT options, and despite a slight decline in 2019, the market has consistently grown year on year. One key trend in Turkey’s pay-TV market is the attempt to transition and develop existing customers. Home broadband penetration continues to grow in Turkey and is a key driver of subscriptions as operators look to bundle pay-TV with broadband to decrease churn for both services. However, the drive to increase broadband penetration and the persistent challenge of exchange rates have caused pay-TV ARPUs to shrink: all operators have a lower ARPU in US dollar terms in 2023 than they did in 2017.

Following Turkey’s 2023 elections and substantial disruption caused by a devastating earthquake in eastern Turkey, operators have raised prices above inflation in 2023, recouping some of the exchange rate depreciation. Maintaining their subscription bases while restoring ARPU will be a persistent theme across Turkey’s pay-TV landscape in 2024 and onward.

Turkey’s regional inequality in infrastructure and income is persistently high, so operators will continue to offer low-cost or low-connectivity packages alongside those that will provide increased revenue but have sought to develop their customer base, nonetheless. Turksat’s basic package currently costs around $2, reflecting its status as a mass entertainment provider. Turksat has continued to upsell more of its customer base to a premium package and has attempted to modernize its customer base through online billing. Turkcell TV+’s IPTV solution is the country’s fastest-growing provider and now has 1.3m subscriptions. Tivibu has seen an increasing share of its total business shift to IPTV; by 2028, more than 85% of customers will be IPTV users.

Other operators have chosen to focus on lower-cost solutions. D-Smart has seen its subscription count decrease in 2022 and 2023, a trend that is likely to continue. A core element of D-Smart’s strategy is heavy discounting of the price of its TV packages when bundled with internet, leading to low ARPUs as the company tries to increase its fixed broadband customer base. Turkcell meanwhile sought to exploit high inflation for commercial gain. After holding its TV+ ARPU at between $1 and $2 between 2017 and 2021, Turkcell TV+ saw a substantial decrease in 2022, in part because the operator sought to gain a competitive advantage through campaigns that sought to combat inflation.

Advertising

Overall, Turkey’s advertising market is set to shrink slightly to $3.6bn in 2023, a decline of -5.3% from 2022. Advertising revenue in 2023 was affected by the earthquake. Online advertising is the dominant form of advertising across Turkey, accounting for 72% of all advertising revenue. Turkey will be the world’s 21st-largest advertising market in 2023 and is forecast to become the 17th largest by 2028. Between 2023 and 2028, Turkey’s advertising market is set to grow at 12.2% CAGR in US dollars, well above the global average of 7.7%.

We forecast Turkey’s video advertising market to grow from $953m in 2023 to $1,135m by 2028. Mobile advertising is the core element of this market and will continue to account for around 85% of advertising revenue in the country. Online video advertising is set to grow by 0.8% in US dollars in 2023 to $678m, a substantial increase in lira terms. We forecast online video advertising to grow at a 10.9% CAGR between 2023 and 2028 in Turkey. In addition, Turkey is one of the leading TikTok markets globally.

Daoud Jackson is Omdia’s senior analyst, media & entertainment