DTVE Data Weekly: Pay TV vs online video subscriptions

Source: Omdia

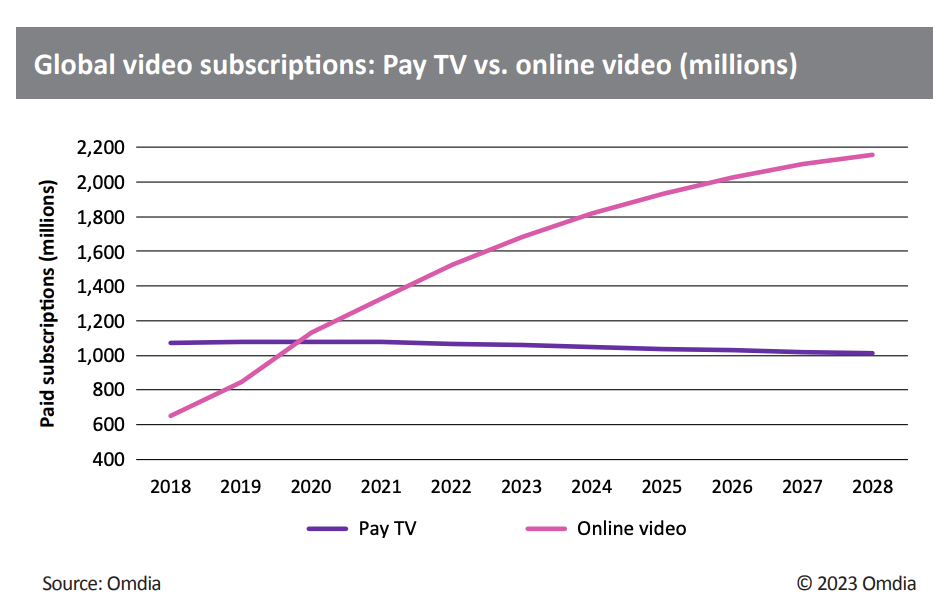

Global pay-TV subscription numbers declined by 1.2% in 2022, from 1.08bn to 1.07bn, with competition from online video remaining an ongoing challenge. Omdia expects the pay-TV market to exhibit a slow decline and forecasts subscriptions to drop from 1.07bn to 1.01bn in 2028, down by 5.2%. The scenario differs a great deal from country to country, however. Omdia tracks pay-TV subscription data for 98 countries worldwide, and the 2022 outcomes show significant fluctuations, with 49 countries reporting subscription growth, 42 reporting declines, and seven essentially unchanged.

By comparison, online video subscription numbers are growing almost everywhere, and the global total increased from 1.33bn at the end of 2021 to 1.52bn at the end of 2022, up 14.8%. Omdia’s current forecasts project the end-2028 figure to be 2.16bn, representing a 41.5% increase from end-2022. With most major online video services having carried out the majority of their global rollout plans, Omdia does not expect to revise that 2028 total due to the announcement of significant new expansion plans. With pay-TV subscriptions still exceeding 1bn globally, Omdia expects the global total of pay-TV and online video subscriptions to top the 3bn mark from 2026. The global total of online video subscriptions continues to rise worldwide, increasing by 14.8% year-over-year (YoY) to exceed 1.52bn by the end of 2022. The online video total first overtook the pay-TV total in 2H20, when it also passed the 1bn subscription mark. Omdia’s current forecast indicates online video subscriptions will total 2.16bn in 2028. A landmark will be reached in 2027, when the online video subscription total will reach double that of pay-TV subscriptions.

The global online video subscription total increased by 44.9% in 2017, 40.1% in 2018, and 29.8% in 2019— so the rate of increase had been slowing. However, this reversed when online video subscriptions grew by 33.7% in 2020, a spike attributed to the COVID-19 pandemic, with subscription numbers benefiting from a captive audience forced to stay home. In this scenario, the decline to a 17.5% growth rate in 2021 and 14.8% in 2022 makes sense, as the market returned to a more regular pattern of smaller growth increases. Omdia forecasts 10.4% growth for 2023 as increasingly mature core Western markets ensure the rate of increase continues to decline.

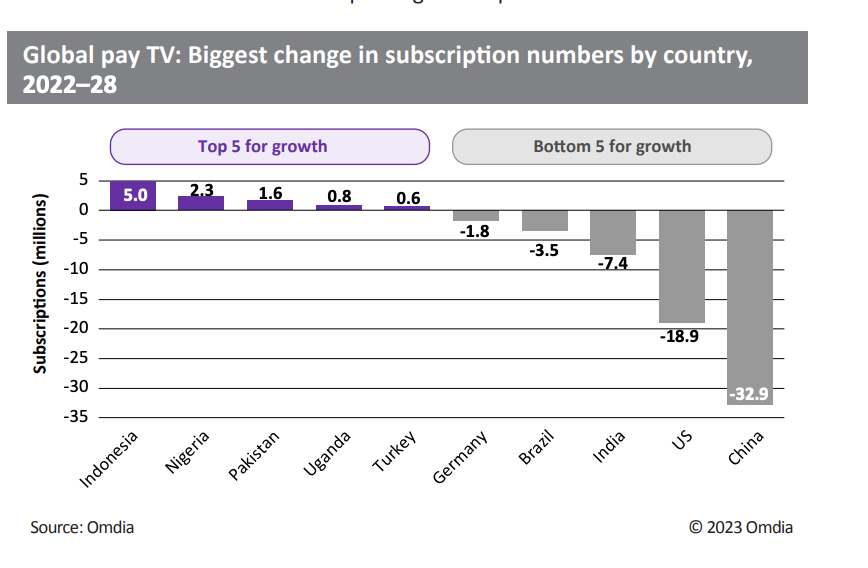

The global number of pay-TV subscriptions— comprising cable TV, digital terrestrial television (DTT), internet protocol television (IPTV), and satellite—hit the 1bn mark in 2017 but has struggled to find significant growth since then. Although Omdia’s forecast is downward, it anticipates only a slow decline, with the sector plateauing globally rather than dropping significantly. The picture locally differs from country to country, with big losses in some markets such as the US, Japan, and Germany offset by ongoing significant growth in countries including Indonesia, Nigeria, and Turkey.

Revenue decline and Monetization

Although there has been a rapid rise in the online video customer base, subscription revenue generated by online video providers remains some way behind pay-TV operators, and this will continue throughout the forecast period. Global pay-TV revenue totaled $210bn in 2022 compared to $111bn for the subscription online video market.

Market conditions vary from country to country, but generally, the success of online video has been built on a flexible, value-for-money offering that contrasts with the rigid, higher-cost model of classic pay TV. But having now exploited the public’s dissatisfaction with pay TV to build up an enormous base of online video subscriptions, the focus will be on how to monetize those subscription bases most effectively.

Numerous factors influence the monetization equation. The first is to acknowledge that a great deal of online video’s success is built upon heavy investment in content acquisition and creation. In 2022, we started to see some acknowledgment that such investment could not continue forever, with some services cutting back expenditure. Fulfilling the public expectation for regular new content was proving to be an expensive proposition and has naturally led to online video services needing to charge higher subscription prices to fund the provision of that content. This comes with a risk, with some customers willing to churn away from these services for the same reason they canceled their traditional pay-TV services: its excessive price.

An alternative to increasing prices, however, is to adapt business models. Ad-supported online revenue totaled $176bn globally in 2022. We forecast it to grow by 73% to $305bn in 2028 as services capitalize on the opportunity to use hybrid AVOD/SVOD models to overcome the public’s resistance to increased subscription prices.

Source: Omdia

There were 1.79bn TV households worldwide at the end of 2022. Of those, just over 1bn homes took a pay-TV service, resulting in a global pay-TV penetration rate of 56%. Although it is in an entrenched pattern of moving slowly downward, pay TV is forecast to remain an important segment globally for the next five years and beyond. The cord-cutting process varies from country to country, with some territories still showing growth in classic pay TV, while mature, developed markets are shedding subscribers more quickly, with much higher ARPU being a factor driving customers more swiftly to cheaper online alternatives. Pay-TV penetration remains high in several key territories, including France, Canada, and India, each with over 70% pay-TV penetration at the end of 2022.

Online video overtook cable TV as the leading single platform in 2018, with IPTV overtaking satellite in the same year. Since then, the platforms have retained their positions in the global rankings, although IPTV’s ongoing growth, coupled with cable’s decline, means that IPTV is closing in on cable—although it will still be some way behind (349 million versus 427 million) at the end of the forecast period. Telcos are in a strong position to employ an aggregation strategy, helping IPTV buck the wider pay-TV trend and continue to grow.

Cable TV accounted for 52.1% of the world’s pay-TV subscribers in 2018, a figure Omdia expects to decline to 42.3% in 2028. Satellite TV, meanwhile, is forecast to drop from a 21.5% share to 21.1% during the same period. With pay DTT playing only a minor role, the big gainer will be IPTV, rising from a 24.7% market share to 34.5% in 2028.

Revenue from pay-TV and online video services, excluding advertising, reached a combined $285bn in 2018, rising to $322bn in 2022. Omdia forecasts this figure will reach $351bn in 2028. Pay TV’s revenue share has declined from 84% in 2018 to 65% in 2022 and is forecast to fall to 53% in 2028, as online video subscription revenue growth continues to eat into its dominance. Based on the current trend, total online video revenue will likely overtake pay TV in 2030 or 2031.

Pay-TV ARPU has declined globally in recent years as operators offer reduced-price packages as an alternative to online video. Although some level of decline continues, the picture is flattening out, with no additional significant ARPU declines forecast. Online video ARPU is creeping up only slowly, affected by pricesensitive customers that may churn away from services that impose significant price increases.

Adam Thomas is Omdia’s Senior Principal Analyst, TV & Online Videos