After more than 40 years of operation, DTVE is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

DTVE Data Weekly: Hybrid streaming tiers – revenue, subs, and monetisation

All major direct-to-consumer (D2C) streaming services in the US have launched some form of advertising element to their business, whether it be a hybrid tier or live sports features with advertising.

Many services have confirmed that customers on the ad tiers have higher ARPUs than customers on non-ad supported tiers. This encouraged many SVOD services to pursue an ad strategy in tandem with their streaming businesses.

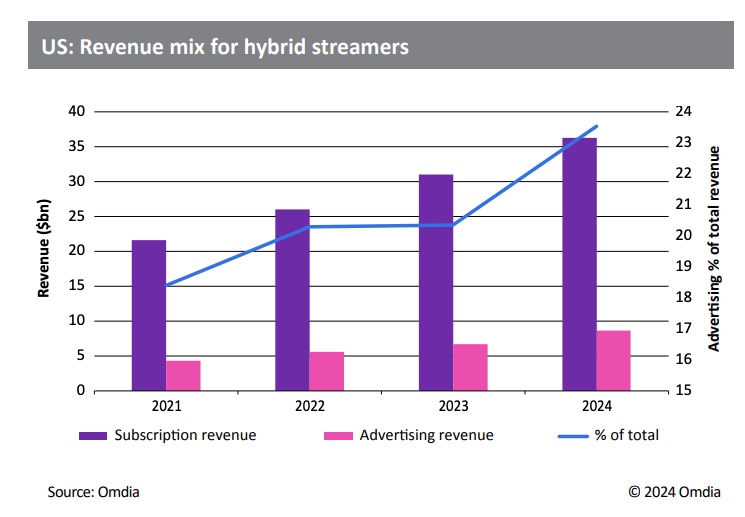

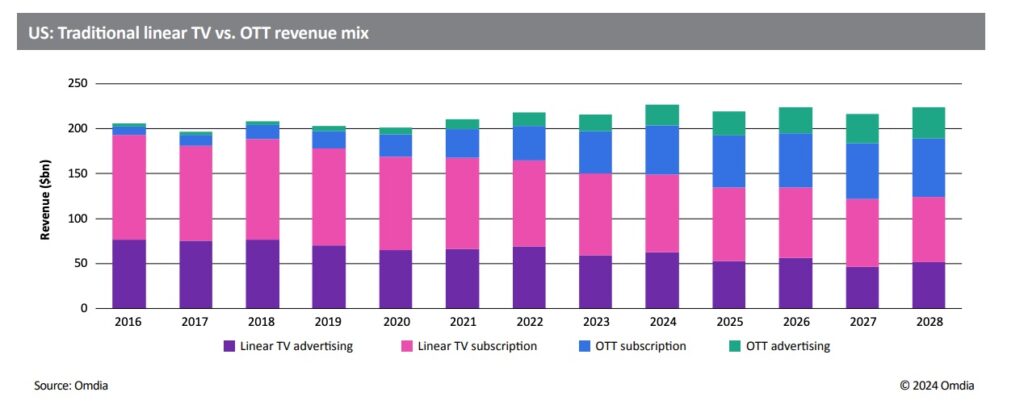

Omdia expects advertising revenue for premium streaming services to reach 19.3% of mixed service revenue in 2024, up from 17.7% in 2023. While this remains a growing part of the business, subscription revenue continues to make up the majority of streaming revenue. Ad-supported tiers are also becoming a popular tool to satisfy consumers looking to churn down to lower-cost streaming or to funnel in new consumers through partnerships. As consumers shift from linear pay TV to OTT, 69% of revenue remains within the linear ecosystem. US advertising revenue ebbs and flows with election years due to high investments in political advertising. The Olympics and the rotation of the Superbowl among major networks also create further seasonal fluctuation in ad revenue. Over the next five years, we will start to see some of this cyclicality transfer over to online video.

Omdia expects advertising revenue for premium streaming services to reach 19.3% of mixed service revenue in 2024, up from 17.7% in 2023. While this remains a growing part of the business, subscription revenue continues to make up the majority of streaming revenue. Ad-supported tiers are also becoming a popular tool to satisfy consumers looking to churn down to lower-cost streaming or to funnel in new consumers through partnerships. As consumers shift from linear pay TV to OTT, 69% of revenue remains within the linear ecosystem. US advertising revenue ebbs and flows with election years due to high investments in political advertising. The Olympics and the rotation of the Superbowl among major networks also create further seasonal fluctuation in ad revenue. Over the next five years, we will start to see some of this cyclicality transfer over to online video.

A significant portion of linear subscription revenue is paid back to studios through carriage fees. The content and studio owners are essentially double dipping on revenue streams by earning through the D2C streaming subscriptions and carriage fees. While content in past decades used to be made with linear ad breaks in mind, now OTT content is more often designed to be binged and needs to account for how ads are integrated into the OTT experience. The hybrid model offers value in several ways:

Reduce churn and increase return: Hybrid advertising tiers allow for lower subscription pricing by integrating advertising into streaming services. Lower prices offer more choices to consumers, providing an opportunity for lower churn or the trading down of tiers to continue subscriptions.

- Tapping into new advertising budgets: OTT advertising offers more data and targeted ad opportunities that previously could not be tracked in the linear ecosystem. Simultaneously, social platforms YouTube, Facebook, and now TikTok grew the online advertising revenue opportunity, largely by tapping into the performance budgets of small and medium-sized businesses (SMBs).

- Hybrid streamers are particularly well-positioned to tap into brand advertising budgets earmarked for TV. Streamers also have an opportunity to tap into performance ad budgets and potentially even retail media ad spend, particularly if shoppable ad formats take off.

- Diversified revenue: In the 2010s, SVOD or subscription streaming services, including market leader Netflix, solely earned revenue via subscriptions. The D2C streaming movement in the early 2020s introduced the traditional TV model of blended ad and subscription revenue to mainstream models. Hybrid models existed before but gained popularity over the past few years.

- Price flexibility: In the linear TV ecosystem, price variances typically surround differences in channel count or carriage. OTT tiers, on the other hand, are leaning into ad-free versus ad-supported, with mostly content parity across tiers. The addition of advertising offsets some subscription costs that would be pushed to consumers, thereby offering them choice and price flexibility

Omdia anticipates that over the next five years, premium ad-supported streaming services will experience a near-zero-sum game with traditional linear TV. All major channel groups are looking at their D2C streaming services (typically hybrid services, with the exception of Fox Corporation’s Tubi) to offset losses in traditional linear TV ad revenue. TV upfronts are now firmly a “converged” TV event: in addition to all channel groups showcasing their combined traditional linear TV and streaming offerings, the 2023 program also featured YouTube and Netflix.

The convergence of traditional TV and online video advertising is raising the stakes for the reform of ad measurement and TV buying currency. The TV network uproar at Nielsen’s attempt to supplement Thursday Night Football measurement with Amazon’s first-party data highlighted that Nielsen’s current methodology strongly underreports viewer migration to streaming. At the same time, the D2C divisions of the major channel groups are actively seeking a transition to a multi-currency regime. From early 2023, NBCU has spearheaded The Joint Industry Committee (JIC), an industry consortium that aims to create a standards and certification system for various measurement vendors and solutions. Paramount, TelevisaUnivision, and Warner Brothers Discovery also support the JIC.

Whether the US market will abandon the Nielsen GRP as a single currency is not yet obvious. Although a multi-currency regime has many appeals, including the modality and flexibility to pick the best point solution for a particular campaign, debasing the single currency carries risks. Agencies frequently see ad measurement innovation as a pretext to demand discounts on what they interpret as underperforming inventory, which can lead to a reduction in the average effective CPM on the market.

However, it is also important to bear the influx of digital-first advertisers into the converged “new TV” ad marketplace. This means that connected TV (CTV) and traditional linear TV will not be a zero-sum game.

Many of these advertisers are SMBs that would not have met the ad spend threshold to advertise on traditional TV (particularly national TV) but can now find equivalent CTV ad inventory available to them.

In addition, digital-first advertisers do not have institutional inertia and loyalty to Nielsen GRP. Although agencies and big brands require the capability to reconcile reporting across all their media partners (hence the support for single currency), the SMB’s data and measurement needs are somewhat different. Automation, self-serve tools, and easy first-party data integration are essential to successfully utilizing SMB ad budgets. It is, therefore,

no surprise that many of the channel groups and their hybrid services now offer (or plan to offer) such functionality.

At the same time, SMBs have long been the prime source of growth for the digital giants Google, Meta, and, most recently, TikTok. In 2022, the meteoric rise of TikTok put breaks on YouTube’s and Meta’s

growth. In 2023, Meta regained its stride in mobile ads, while YouTube redoubled efforts to grow its CTV business. This means that YouTube is one of the most important competitors to hybrid services; it has particular strength when it comes to service SMB advertisers, but it, too, has been eyeing traditional TV budgets for many years.

CTV platforms—Roku, Vizio, LG, Samsung, Google TV, and Amazon’s Fire TV—are the gatekeepers of the “new TV.” Positioning and discoverability in the CTV UI will be critical to streaming services’

success. All these platforms also run owned-andoperated premium ad-supported services (typically FAST services). This means that the CTV platform relationship with hybrid streamers is a complicated and multifaceted interplay of service carriage and UI positioning, UI ad purchases, ad inventory sharing, content licensing, ad tech and first-party data sharing, and direct competition for ad budgets.

Although AVOD companies are the primary players in this space, in the future, it is likely that curated FAST channels and simulcast programming will be prioritized for premium SVOD services. Peacock, Paramount+, and Max have integrated versions of FAST channels or linear TV simulcasts into their platforms. However, they are not prioritized on the main page UI and are sometimes not even branded as channels.

When content is simulcast versus FAST, it means that it is a live feed from the traditional linear TV channels, and typically, ad placements and revenue are mimicked with whatever airs on traditional linear.

Sarah Henschel, is Omdia’s Principal Analyst, Media & Entertainment