DTVE Data Weekly: Federated CDN shows promise for ISPs

Content delivery networks (CDNs), in both private and public deployment models, have been instrumental in enabling streaming over a public internet infrastructure that was not configured to do so at its inception. By providing capacity where ISPs cannot, CDN service providers support SVOD and online video more broadly.

“Broadcast-grade” streaming, however—defined as consistent end-to-end latency of less than 5 seconds with the sort of “one-to-many” network efficiency that broadcast architectures boast—remains elusive in many instances. To support broadcaster migration from legacy distribution models, ISPs and public CDNs are looking for ways to deliver broadcast-scale events over the internet with high quality of experience (QoE) through deeper, country-level caches.

“Broadcast-grade” streaming, however—defined as consistent end-to-end latency of less than 5 seconds with the sort of “one-to-many” network efficiency that broadcast architectures boast—remains elusive in many instances. To support broadcaster migration from legacy distribution models, ISPs and public CDNs are looking for ways to deliver broadcast-scale events over the internet with high quality of experience (QoE) through deeper, country-level caches.

Telco operators are taking the initiative and are looking to develop services that will enable them to improve traffic management practices for content delivery; the Open Caching (OC) specification heralds a potential path for ISPs to serve OTT providers that have not developed proprietary CDN infrastructure in the same way Netflix has. Network surges, particularly with live sporting events and large gaming releases, although few and far between and not a large share of overall traffic, place significant pressure on telcos at multiple points in the network chain—something likely to continue as more TV is consumed via streaming.

For example, BT in the UK disclosed that average peak traffic increased to 28 terabits per second (driven by video consumption) at its busiest period during 2022, up by 10% from the previous year and over two-and-a-half times the 2018 level. This increased pressure on operators keeps CDNs relevant, as they help manage the load by caching popular content closer in the network to end users (i.e., improves performance without adding network strain), in turn lowering the service provider’s impact on external links, keeping costs down.

OC functions by placing servers deep into ISP access networks; then, using standardised APIs, servers source OTT content from upstream CDNs and cache more locally rather than transiting content across peering points and IXPs. It promises to reproduce a broadcast-like traffic pattern in ISP networks, and, given that it functions like a software umbrella connecting multiple CDNs, it de-complicates and optimises OTT content delivery while ensuring improved QoE for end users.

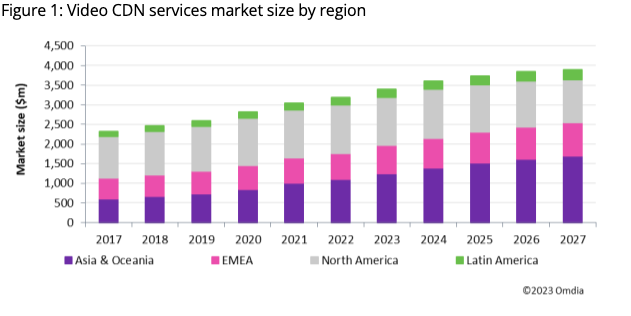

CDN services market

Stakeholder analysis is important here. The OC initiative (driven by industry group the Streaming Video Technology Alliance) spans the whole value chain: CDN appliance and software vendors (e.g., Broadpeak, Ateme), managed CDNs (Edgio and Qwilt, among others), ISPs (notably Verizon and Telefónica), and major content providers (chiefly Disney). Conspicuously, those not participating in the initiative include Akamai, which built a business primarily through stacking capacity at network peering points—a different model.

If OC gains traction, large public CDNs like Akamai could stand to lose out as they rely on proprietary technology catering to content providers rather than ISPs, which might prefer to reduce their reliance on public CDNs. Moreover, their services typically end inside of ISP headends or hubs, and they could find themselves competing with ISP-operated delivery services deeper in access networks. More importantly, Akamai’s main focus lies in building out its cloud computing capabilities and developer solutions.

Qwilt (with the backing of Cisco, notably) has been especially active in trying to establish the OC standard among ISPs. To date, more than 150 service providers have partnered with Qwilt, with the goal of creating a globally federated ISP-based CDN network. This is not new: Edge Gravity signed several dozen broadband providers before Ericsson pulled the plug in 2020, but Qwilt seems to have made more consistent progress.

Statistics

The global CDN services market had a solid year in 2022, growing by 2.9% to $3.3bn. This is a drop-off from the 8% in 2021 as the North American market had a particularly slow year due to increasingly consolidated media buyers having greater leverage to pressurize public CDNs on price. Revenue growth is projected to continue but at a steadier rate than the period 2017 to 2022, growing at a 4.1% CAGR over 2022–27.

The CDN appliance and software market is much smaller—around a tenth of the size of the CDN services market—but is growing at a faster rate. Over the year to 2022, this market grew by 22% to $283m. This was driven by three things: operators transitioning to installing out their own CDNs at the edge as a cost-saving alternative to managed CDNs; their legacy IPTV systems reaching end-of-life and becoming expensive to maintain; and operators looking to mixed deployment models of on-premises as well as cloud. This trend is set to generate a 9.8% CAGR from 2022 to 2027, which will take the market to a revenue of $431m.

In the CDN services market, North America accounted for $1.23bn, 40% of all public video CDN revenue, but Asia & Oceania registered a 10% annual growth rate in 2022: factors such as higher bandwidth delivery and the relatively rapid growth of public cloud are driving the rise of large Chinese and wider APAC CDN vendors. This region contributed $1.1bn in 2021 and is forecast to grow to the $1.4bn mark in 2022. The Europe, Middle East & Africa (EMEA) market grew to $658m revenue in 2022 and is forecast to contribute $735m in 2023.

Commercially speaking, it is early days for OC. ISPs may open a new line of business by charging content providers for delivery services over the last mile of their networks. Orange has been a nascent example, launching a commercial CDN in France last June as a local offering for content providers wanting a high standard of QoE. Whether this can scale for telcos is unclear, and many operators find it perfectly straightforward to resell a global CDN.

However, as national and local broadcasters look to phase out legacy distribution models over the next decade, this is an element of the value chain that ISPs could be well positioned to capture.

Thomas Thomson is Omdia’s senior analyst, Video Technology. Read the full Video CDN Market Report – 2023 Analysis here.