DTVE Data Weekly: Consumer bundling — the era of reaggregation

Source: Omdia

Over the last few years, media consumers worldwide have witnessed the launch of many new online video services, each seeking to claim the hearts and minds of their audiences, akin to the rise of Netflix in the mid-2010s. Much of this growth was facilitated by new partnerships and alliances with local service providers to create enhanced media offerings in an increasingly widespread format in a manner that consumers were growing accustomed to.

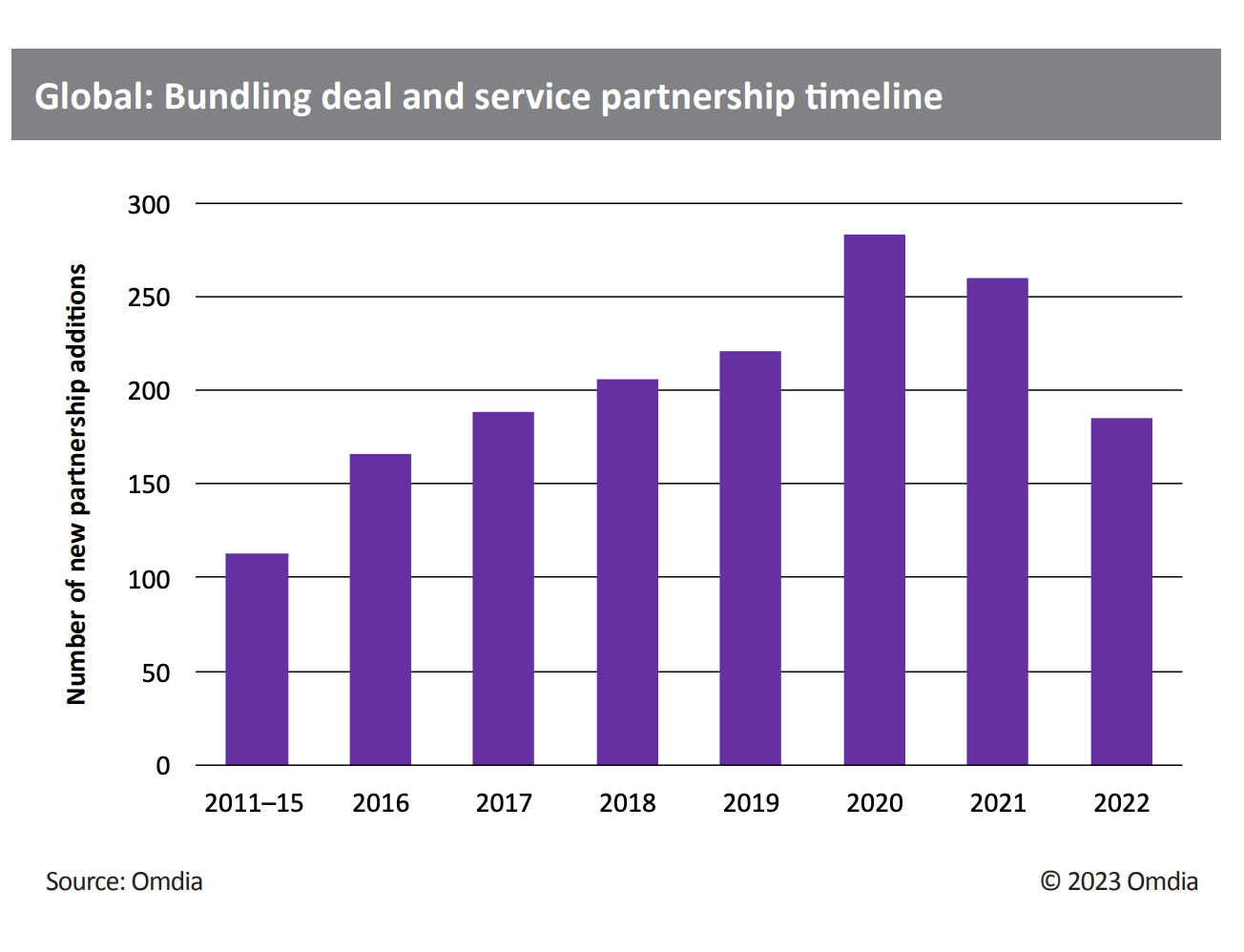

The Omdia OTT Video Bundling and Partnerships Tracker has observed the number of new partnerships rise from just over 100 between 2011 and 2015 to more than 200 per year from 2018 onward. This total has continued to expand, and there are now more than 1,200 live partnerships as of 1Q23. Beyond these, however, there are many more partnerships in the fields of online channel aggregation, cloud gaming, and retail bundles. Furthermore, there are new discussions of how hybrid video services and tiers and purely ad-supported video services can fit into this bundling and aggregation model.

This increasing complexity signals a more in-depth understanding of the interconnected nature and fortifying effect of all media and entertainment sectors. An era of mergers and acquisitions and a heightened focus on distinctive and unified branding has seen renewed attention paid to how to satisfy customers’ fundamental quest for a broad range of media at a reasonable price point. However, consumers are less interested in the source of content than in the content itself. According to the Omdia Consumer Research survey, 46% of respondents cite paying for multiple video services through one bill as important to them, versus 80% citing price. Only the quality of experience in accessing this content matters to the end user, a feature historically facilitated through pay-TV and media packages.

Gaming and ad-supported content

Advertising-supported and gaming content, two major themes of the video industry, are also fueling the future of bundling. Gaming, in particular, has been in the spotlight following recent success with video game–focused IP in the cinema and on TVs at home. Data from Omdia Consumer Research shows that 87% of gamers also use an online subscription video service, and 67% have a pay-TV service, highlighting a valuable cross-section that service providers have yet to readily explore. Meanwhile, increasing free/AVOD service stacking and consumer affinity for video content supported by advertising should not be mistaken as binary consumer preference for engaging with content in this way. It is instead the result of the ongoing tradeoff between the price one is willing to pay to access content and the level of disruption one is willing to endure.

A more in-depth level of bundling also plays into the hands of the increasingly seasonal nature of media consumers and how, as their options have grown, the number of choices they make has also grown. As time goes on, consumers will be increasingly aware of the state of their media and entertainment portfolios. Consumer inertia will be much less of a factor in media service ownership as macro and socioeconomic factors drive additional and more in-depth decision-making. Service providers that can serve this consumer need will reap the rewards of longer-term platform engagement and the capture of consumer revenue as it moves around. With Omdia forecasting that 25% of online video subscriptions will come from partnerships by 2028, the potential reward for disrupting the partnership space is massive.

Max Signorelli is principal analyst at Omdia, Media & Entertainment