What are the prospects for FAST in central and eastern Europe?

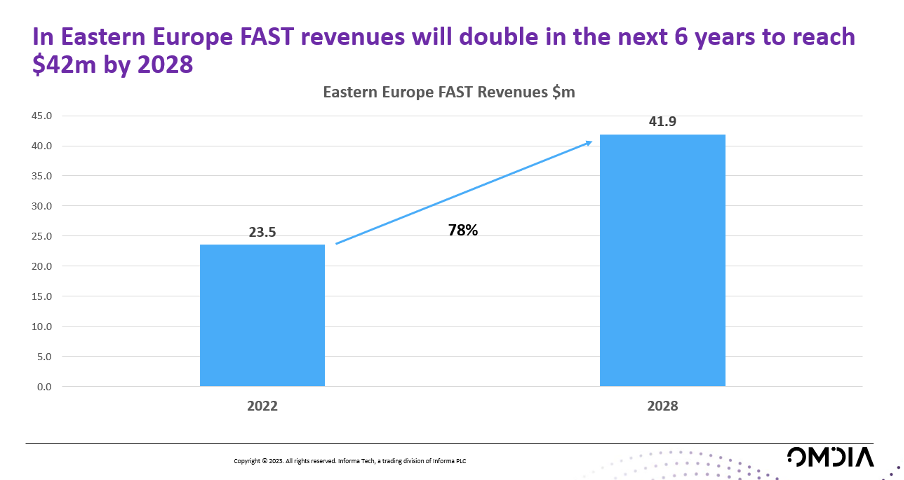

In central and eastern Europe, FAST revenues will double in the next five years to reach US$42 million by 2028, according to Omdia’s forecasts.

That means FAST will remain a very small part of the overall advertising picture.

That means FAST will remain a very small part of the overall advertising picture.

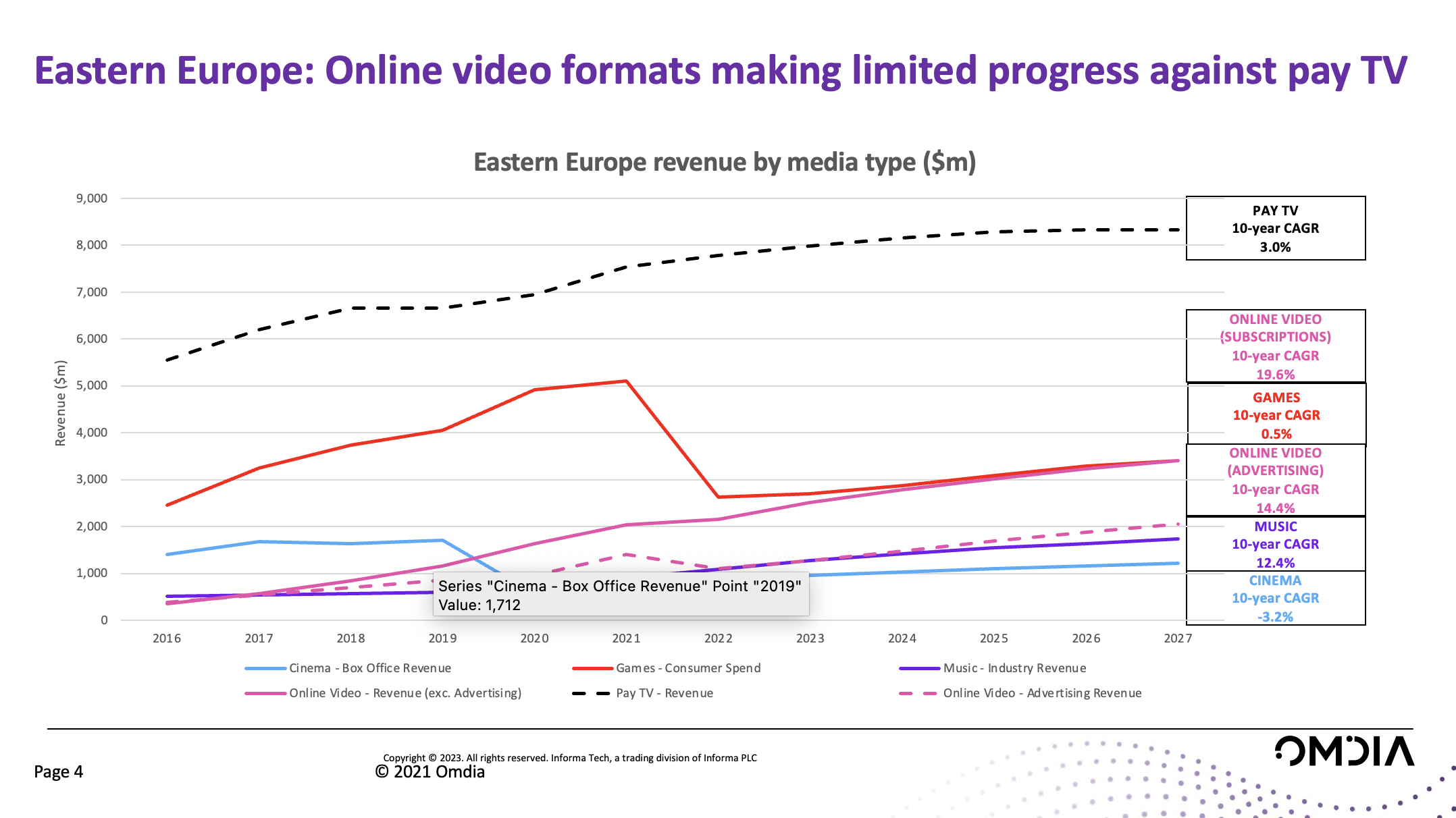

Traditional linear TV and social video continue to drive video advertising revenues in eastern Europe with revenues of US$5.6 billion and US$1.1 billion respectively.

Pay TV is still growing in CEE and traditional free-to-aid viewing is also strong, so there is less consumer interests in FAST. At the same time the online advertising market is a lot less developed compared to Western Europe, so there is no ecosystem or marketplace (yet) to support premium ad-supported AVOD and FAST services.

In terms of FAST platforms, CEE is dominated by Rakuten and Plex. None of the other global platforms are present in the region as of yet – there is no Pluto TV, no Samsung, no LG.

In terms of FAST platforms, CEE is dominated by Rakuten and Plex. None of the other global platforms are present in the region as of yet – there is no Pluto TV, no Samsung, no LG.

There are some local players such as Kabaret TV in Poland, but overall, FAST remains very nascent in CEE.

Localisation costs

Dubbing costs are also a big inhibiting factor in the economics of FAST channels.

Until the market is big enough the international FAST channel operators are unlikely to launch their channels because they won’t cover the cost of dubbing. ITV Studios cited this as the reason they haven’t launched in Italy or Spain. Given that calculation, the more fragmented markets of central eastern Europe, with multiple languages, will be even further behind when it comes to localising FAST channels.

AI-based dubbing is something certain channel operators such as DAZN are looking into to limit the costs.

However, this inhibitor also underlines the extent to which FAST remains a low-cost business where providers look to keep upfront investment to a minimum. In terms of the overall content business in a market such as CEE, FAST remains something of a backwater.

Maria Rua Aguete is senior research director, media and entertainment at Omdia.